Learn the six senior tax breaks that apply to retirees or affect seniors because of their retirement status or age. First, I cover the six tax breaks then show you an example of how to apply them.

It is inherently easier for retirees to control their tax bill and thereby take advantage of specific senior tax breaks. Unlike working people who get the bulk of their income from wages (taxed at the highest rates as ordinary income), retired seniors get much of their income from Social Security and investments. By changing investments and the investments you tap for income, you control your tax bill.

(c) Can Stock Photo

Immediate Annuities Income Source for Those 60+

A person of any age can buy an immediate annuity but they usually make no sense for pre-retirees. And in this era of low-interest rates, they make no sense for someone under age 70.

The idea is simple. You make a deposit with an insurance company and in turn, they send you a monthly check for life. The purpose of this post is not to explore details of immediate annuities. Rather, I want to show you the tax break offered.

Immediate annuities pay a consistent income and because the payments are based on age, they only make sense for people age 60+ to use these vehicles (the higher the age when you invest, the higher the payment--see the immediate annuity calculator). They also make the best sense when interest rates are high as you will lock in a higher monthly payment. Let me explain the tax break.

The senior tax break is that IRS taxes immediate annuity income in an odd fashion. The IRS considers some of the payment return of principal (untaxed) and some of the payment interest (taxed). For an investor age 60+, 60% or more of each payment will not be taxed (unless the investor exceeds their life expectancy in the case of a life annuity). The fact that IRS excludes a portion of the payment from taxation is one of the nice senior tax breaks.

Let's consider an example using the data in the table below. A male invests $100,000 for the following returns [Comparative Annuity Reports October 2016, highest immediate annuity rates]

| Age (male) | Monthly Lifetime Income | Income Excluded from Tax |

|---|---|---|

| 60 | $462 | 71.5% |

| 65 | $530 | 74.8% |

| 70 | $624 | 78.5% |

| 75 | $754 | 82.5% |

Therefore, a 70-year-old male purchasing the annuity will receive $7488 annually and in the 25% tax bracket, pay only $402 tax on that income. (If the senior citizen lives beyond his life expectancy of 87, the income becomes 100% taxable).

How Much Tax You Pay on Social Security Income Is Up to You (in many cases, pay NO tax on Social Security Benefits)

Seniors pay tax on only part their social security benefits.

The portion of social security income that is taxed can vary from 0% to 85%, based on the senior's total amount of income AND the components of that income. Since only people age 62+ receive social security retirement benefits, we can certainly consider this one of the major senior tax breaks.

I might mention here that IRS does not tax all income equally. It is critical to understand that how you organize your affairs determine how much tax you pay. Specifically, the types of investments you choose and where you buy those investments (inside or outside of a retirement plan), determine how they are taxed. Here's a summary chart:

| Type of Asset | Where Held | Tax Rate |

| common stock or real estate | not in a retirement plan - held more than one-year | capital gains rate for most people is 15% and is often 0% for many seniors (depends on total income) |

| dividends on common stock | not in a retirement plan | same as above |

| common stock or real estate | held in a retirement plan | will be taxed up to 39.6% when withdrawn from the retirement plan |

| dividends on common stock | held in a retirement plan | same as above |

| mutual funds | not in a retirement plan | taxed annually even if you do not sell shares - some gains will be short term (up to 39.6%, some long term usually taxed at 15%) |

| mutual funds | held in a retirement plan | will be taxed up to 39.6% when withdrawn from the retirement plan |

Retirees can manage their finances to reduce taxes on their social security benefits by moving money from assets that increase total income (CDs, bonds, tax-free bonds, savings bonds) to deferred annuities or immediate annuities, some or all of the income from which does not appear on the tax return. These investments lower the total income appearing on the tax return and thus the percentage of social security income subject to tax. Our post, Taxation of Social Security Benefits explains in detail with an example

Slow the Pace of IRA/401K Distributions

Senior citizens age 70 1/2 must take distributions from their IRA, but above a minimum required amount, they can decide how much to take. The less they take, the less tax is paid today.

Over the last 10 years, the government has reduced the minimum amount that needs to be taken creating a tax break for seniors. As a senior, you can manage your finances to take just the minimum required IRA distribution and using non-IRA assets for living expenses.

Here is one of the newest senior tax breaks for slowing down taxable distributions. The IRS gives favorable treatment to a Qualified Longevity Annuity Contract (QLAC) in your IRA as distributions are not required until age 85. Two limitations:

- only 25% of retirement accounts can be invested into a QLAC

- the cumulative dollar amount invested into QLACs cannot exceed $125,000

Whether a QLAC is appropriate for you as an investment requires considering factors other than deferral of those taxable required minimum distributions.

"Ordering" Will Help Reduce or Eliminate Your Income Tax

It's likely you may not have heard the term "ordering." Your financial advisor may not have mentioned this as it does not give rise to his opportunity to make a sale. Additionally, he is not supposed to provide tax advice (he is prevented by his firm). And unfortunately, I doubt that most CPAs bother to mention ordering.

If you spend your IRA money, you may pay up to 39.6% federal tax (or even more in some cases) on that IRA withdrawal (plus state income tax). But if you spend $1 from your savings account, you pay no tax to withdraw that money. The IRS taxes IRA withdrawals as income but withdrawals from your savings account are from income that was previously taxed and does not get taxed again.

Therefore, as a senior, you live on different parts of your nest egg and you can control your tax bill. You decide whether to take money from one pot or the other. Working people living from salary do not have this flexibility as all or almost all of their income is from wages. As a general rule, spend principal before you spend funds that are tax-free or tax-deferred.

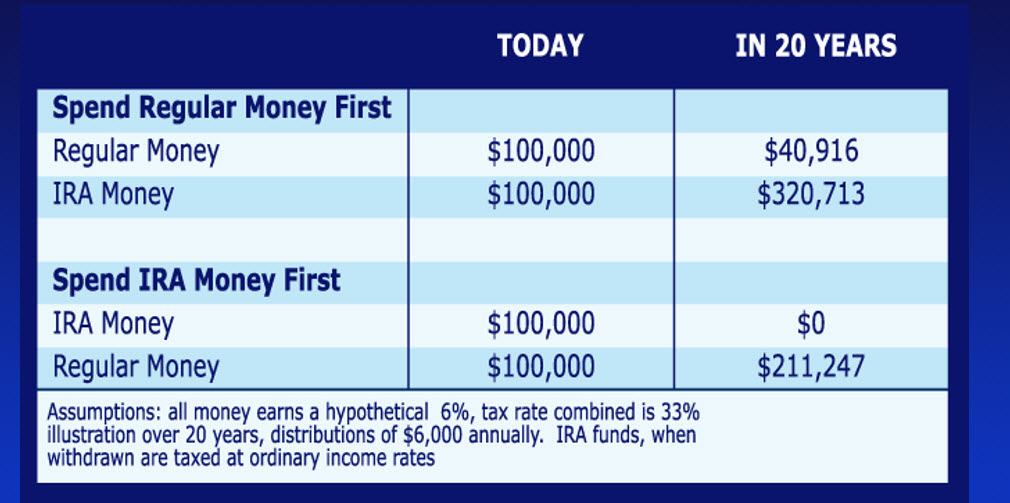

Ordering Example Produces an Extra $150,000

Take a look at this table below. It shows 2 scenarios. Both start with $100,000 in a savings account (regular money) and $100,000 in a traditional IRA.

In the first scenario, the senior investor uses his regular money first and delays tapping his IRA. At the end of 20 years, the investor has a total of $361,000 as the IRA has grown substantially.

The the second scenario, the older investor uses his IRA money first. This money dissipates faster because to get $2 of spending money, the investor must withdraw $3 from the IRA ($1 goes to taxes leaving $2 for spending). The regular money is left to grow as much as possible. However, for every $3 the regular money earns, $1 immediately goes to taxes leaving $2 to spend. The investor's ending balance in this scenario is $211,000 ($150,000 less than in the first scenario ).

Some will argue that the first scenario simply leaves a large tax bill to pay as the IRA has $100,000+ of taxes due when distributed. However, the tax is offset by the fact that these IRA dollars can become a stretch IRA and the fact that the deferral of the taxes for many years has real value and not simply the delay in paying taxes.

The above dictates that the smart investor spends his principal first (the regular money).

Some people may have a problem with the idea of spending principal, but in fact, there is no such thing as "principal." All of your money is green and you won't find "principal" or "interest" written on any of your cash. See for yourself. Take some cash out of your pocket. Is that cash principal or could it be interest income that you earned? Doesn't matter.

Principal is simply a term we humans made up to help talk about money.

Long Term Care Insurance - Two levels of Senior Tax Breaks

The federal government wants older taxpayers to have long-term care insurance so they provide two senior tax breaks as an incentive (see estimated costs using the long term care calculator).

Since the average buyer of long-term care is age 60+, any tax breaks regarding long-term care are essentially tax breaks for seniors. Although not many people qualify for the first tax break, to the extent your out-of-pocket medical expenses and health insurance premiums exceed 7.5% of your adjusted gross income (7.5% for 2016, 10% thereafter), you can deduct that excess as an itemized deduction on our tax return. There is a limit to how much can be deducted but that limit increases with age--in effect an age-based senior tax break.

| Long-term Care Premium Deduction Limits | |

| Age of Taxpayer | 2016 |

| Age 40 or younger | $390 |

| Ages 41 - 50 | $730 |

| Ages 51 - 60 | $1,460 |

| Ages 61 - 70 | $3,900 |

| Over age 70 | $4,870 |

One great idea is to place money into an immediate annuity and have the monthly income pay the premium on long-term care insurance. You take advantage of two senior tax breaks simultaneously. For details, you can read this more detailed post about using an immediate annuity to pay for long-term care.

Want to know more about senior tax breaks?

How to Pay Zero Tax Scenario

(c) Can Stock Photo

Now, let's look at how to apply some of the above information.

Let's assume you are age 65 and married. Your spouse is also age 65. You have income as follows:

Pension $15,000 (taxable)

Social Security $30,000 (partially taxed)

Mutual Fund Distributions $15,000 (taxable)

IRA and 401K Distributions $20,000 (taxable)

Bond Interest $20,000 (taxable)

Home free of debt $600,000 value

Raw Land held for Investment (inherited) $200,000 value

Keep in mind that making financial decisions in the US is complex. What I show you to slash your taxes may not be the best idea for you from other viewpoints such as investment allocation, estate planning, risk minimization, etc. That's why people go to financial planners, as often, these are all competing objectives and you need someone with the wisdom to balance them.

Here is just one hypothetical scenario (and not a recommendation) showing how income tax can be eliminated by married taxpayers with $100,000 gross income, both age 65, filing jointly and using the standard deduction.

The actions taken to get the tax to zero are explained below the table.

| Category | Original Taxable Amounts | Modified Taxable Amounts |

|---|---|---|

| Bond Interest | 200001 | 0 |

| Dividends | 100002 | 4000 |

| Capital Gains | 50002 | 0 |

| IRA/401k Distributions | 200003 | 0 |

| Pension | 15000 | 15000 |

| Social Security | 255004 | 11100 |

| Deferred Annuity | (20000 deferred tax) | |

| Taxable Income | 62,400 | 3,000 |

| Total Tax | 6191 | 0 |

1Bonds replaced with a tax-deferred annuity with the same interest rate. Annuity income is deferred and does not appear on your tax return and is not included in calculation of your social security benefits tax.

2Mutual funds replaced with blue chip stocks to be held indefinitely. Mutual funds provide no tax control due to year-end distributions (which taxpayers had been reinvesting) while stocks generate no capital gains tax until sold.

3Taxpayers have been taking distributions from tax sheltered accounts to supplement income. Distributions ceased and replaced with non-taxable cash flow from either a reverse mortgage, loan against land held for investment or 1031 exchange of land for income producing property.

4The amount of social security that is taxable is dependent on other components of income and the above reallocation has reduced the amount taxable.

Also, keep in mind that deferred tax must be paid at some point. But I hear from sources that it's better to pay when you're dead.

See below for the tax saving cheat sheet or complete booklet to more fully understand and utilize senior tax breaks.

MORE Senior Tax Breaks!

You now see how the six main senior tax breaks can be used to reduce your federal income tax. Our example uses a retired couple with $100,000 income and we are well aware that millions of retired couples have lower income. Therefore, only some of these tax breaks may apply. But there are more.

There are tax credits and also property tax reductions at the local level that are often available to senior citizens. For example, you may now pay property tax on a low assessed property value. Even if you trade down to a smaller home, your property tax could increase. For the elderly, many localities will not assess a higher tax in these trade-down situations. This is a great tax break for older homeowners of any income level.

Questions about senior tax breaks? Use the comment box below.

[clickfunnels_clickpop delay="35" id="8haqcmxhvo2847i3" subdomain="retirement-income.net"][/clickfunnels_clickpop]

You Pay More Taxes Than Necessary

And we guarantee your CPA has never told you The problem with paying taxes is that most people overpay. So if you are concerned about having enough in retirement, you must stop overpaying taxes. I know you think your CPA takes care of this for you. WRONG. I AM a CPA (retired) and I can tell you that 90% of CPAs do nothing more than enter your information into the little boxes on the tax return but NEVER tell you how to pay less next year. Why? Many of them simply do not know what we can show you. In ten minutes.Get Your Copy Now - 6 Ways to Cut Retirement Taxes

A great blog, really impressed, need some more blog like that so that people gets aware form such thing.

Thank you for your article. very useful article.