Save More for Retirement - Shallow Advice

The most simplistic advice you’ll hear about preparing for the golden years is to save more for retirement. It’s simplistic because it requires no thinking. Clearly, if you save more you have more.

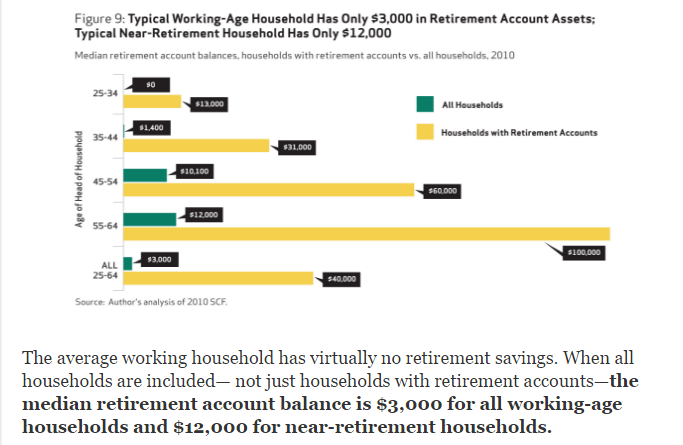

But how good and how workable is this advice? Based on the actual retirement savings of the average household, this advice to save more for retirement has fallen on deaf ears.

Or maybe, people hear this advice and do not have sufficient earnings to save. That appears to be the problem as incomes have lagged far behind expenses, particularly for younger people (i.e. millennials). Indeed, the millennials are burdened with over a trillion dollars of student debt while this was not an issue for us boomers. I had saved $5,000 and my parents contributed $5,000 for the $10,000 total cost of my college education at Penn State (including living expense). I did not borrow any money.

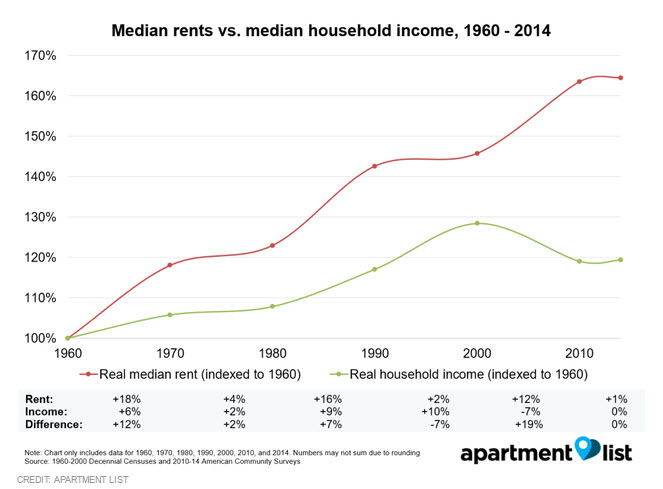

Look below at the struggle younger people have to find an affordable apartment. Salaries have not kept pace with increasing rents.

When I took my first job out of college, I and a roommate rented a 2 bedroom apartment in a luxury complex. We both drove brand new cars (paid for in cash). Our rent was $360 monthly and I was responsible for half. My rent was 15% of my $14,000 annual salary. The current rent for the same apartment in my town is now $3500 monthly. Two people each earning $90,000 would consume 23% of their incomes for rent - 50% more than when I was young.

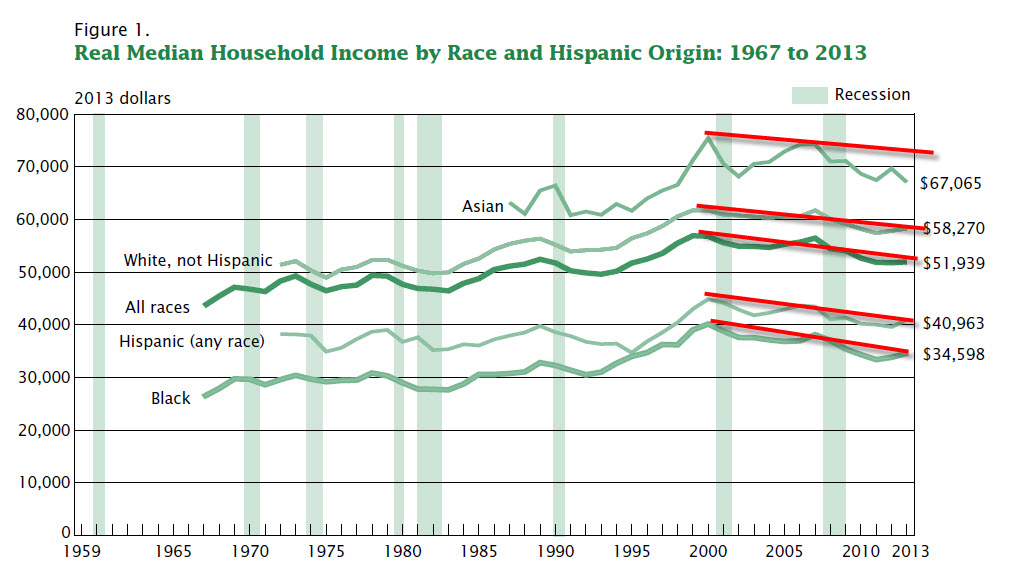

And if we look at incomes overall, we see that our ability to make purchases (i.e. real income adjusted for inflation) has declined steadily since 2000.

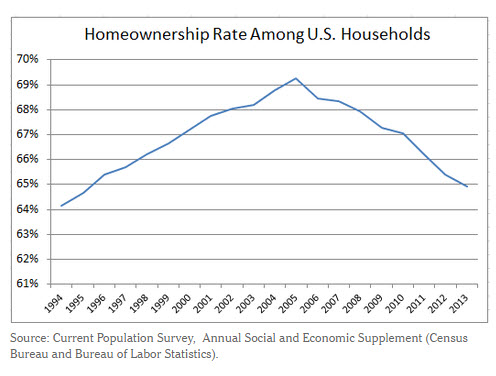

And starting a family and buying a house? Out of the question for most people under age 35.

My argument is that the advice to save more for retirement is just simplistic and unworkable. People have heard that recommendation dozens of times and it’s not that they don’t want to save; they can’t save. They have nothing left after meeting the expenses of a modest lifestyle.

Telling people to save more for retirement is like telling a fat person to eat less. Does that work?

Temporal Perception Prevents More Retirement Savings

Very few people will trade off having a good time today for good time 30 years from now. We simply value whatever we can have today far more than whatever we can have in the future. This is obvious in our behaviors. Most of us overeat or eat the wrong foods (according to CDC, 2/3 of us Americans are overweight). We know it’s not a good idea. We know this could increase disease at older ages. And yet we order dessert today. We have a very high discount rate for our own futures and will always choose pleasure today over pleasure tomorrow.

Ask any smoker if they know that smoking is bad for their health. It is my belief that 100% of smokers know this. Yet they continue to smoke. This is not only evidence that we highly value immediate pleasure, it is also evidence that knowledge has little impact on behavior. So to state that people need to be more financially educated is also bankrupt advice.

You can educate people, you can give them the best savings vehicles, you can stand on your head and the fact is, the majority of the population has a two-week time horizon and wants to know how to have a good time right now.

Mandatory Retirement Savings Is a Good Step

It is possible to have people save more if it’s forced on them.

For example, if the federal government simply levied an additional tax that was actually a contribution to your own retirement fund, you would have no choice. You would end up at retirement age with a nifty nest egg.

I am not talking about expanding Social Security where everyone’s money is mixed into one big pot. That system is a failure. I am suggesting that each person have their own account.

Most people think that they get the largest payment automatically. Not true. You need to make choices when you apply and if you make the incorrect choice, you get a smaller check -- for life. Even if you already receive Social Security Benefits, you may be able to change your selections.

The ramification is that people would need to cut back even further on their living expenses. In other words, they would opt for a lower standard of living today for a better standard of living in the future. Not many people would vote for this.

As I write this, a number of states are considering laws that would force even small employers to offer a retirement savings program. The idea is to expand retirement saving opportunities to more people who do not have a retirement plan to work. The problem is that participation is optional. To work, contributions must be mandatory.

The average person will not willingly cut back on their standard of living to save more for retirement. This is true even when given free money. The American Benefit Institute reports that half of the participants in 401(k) plans with matching contributions do not take advantage of the full matching amount by contributing more of their own pay. In other words, they pass up free money to have more pleasure now or meet non-discretionary living expenses.

If government wants to really help people with their retirement savings, it will need to make those savings mandatory. On the other hand, do we want more government in our lives? Thus, the dilemma.

Look at Retirement Differently

I have suggested that the idea of 100% retirement has been an anomaly. Prior to 1900, there was no such thing except for the very wealthy. For most people, they worked in their fields until they died. It was not until the greatest generation, those who lived through the depression and fought World War II, that full retirement became the norm. This occurred during a small window of time when companies had funds for defined benefit plans and the ratio of workers to retirees was much higher. That period has ended.

We now live in a world that is far less economically robust. In fact, our standard of living is now decreasing. It is almost un-American to say this. America has been the land of continuously increasing standard of living. No more. We have had a party with excess debt and must now make repayment. Expecting people to save more for retirement when their money buys less and less is simply ludicrous.

Companies have done away with their defined benefit plans as they can no longer afford it. Indeed, companies have tried to eliminate labor so as not to fund retirement plans or other benefits. CEOs would like to replace every worker with a robot. Technology is helping them do that.

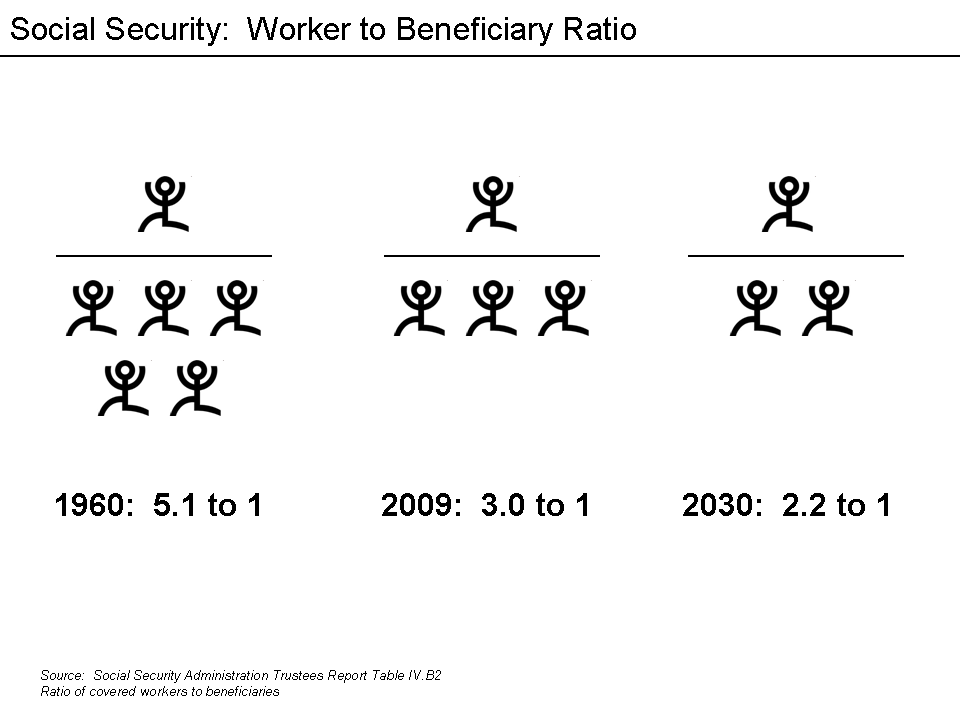

We know that Social Security is in trouble as we are down to 2.5 workers per retirees for the purpose of funding Social Security. And the United States is in far better shape than almost every other country in terms of supporting retirees.

The answer is of course to do away with the outdated view of retirement. The new retirement must include some work as a source of retirement income. Perhaps at age 65, people change from working full-time to maybe 40% time and then retire completely at age 75. Clearly, as lifespans have increased, don’t we need to also increase retirement age?

It is also best if those turning age 65 realize that their employers may want them out the door completely and do not offer part time work. For that reason, those of "retirement age" seeking income must change their thinking about how retirement income is earned and not expect to easily get a job.

You do not need special talents, skills, computer knowledge, etc. We show you multiple ways others are working a few hours a week to generate a comfortable retirement income.

To think that the average person can save all that they need by age 65 for a full retirement is not workable. To save more for retirement is a good idea but not a workable solution for retirement. I would like to ask financial planners, financial institutions and financial journalists to stop making this recommendation.

Save More for Retirement - Fahgetaboutit

You can’t save more for retirement when you’re already 58.

(c) Can Stock Photo

Isn’t it infuriating to see all of those articles targeted at young people to save more for retirement?

How does that help you when you’re a few years away from typical retirement age and you have little to no retirement savings?

The reason you see so many articles about saving more is because that is brainless advice that requires no thinking whatsoever. In order to explain how to have a retirement when you’re already close to retirement age, requires some creative thinking.

Let’s consider the alternatives.

You never retire completely, you just slow down or work seasonally

If you work 40 hours a week currently, can you shift to 20 hours a week in retirement, reduce your income and enjoy some free time? Or maybe better, can you shift to seasonal employment so that you only work some months of the year?

People that have businesses or jobs at resorts typically work only during the “high season” at the resort which may be summer or winter. For example, I have a friend who is a chef and he works four months every year for a six-figures at an expensive resort. While having a skill gives you more options, you don’t need any skills to pursue this strategy.

Any resort needs to hire labor during high season. That labor is typically unskilled meaning you don’t need any special degrees, education are training. Simply being a waiter or waitress can pay very well when you decide to work 80 hours a week for four months and take the other eight months off.

Don't dream about a vacation in Hawaii. Get a summer job and live there for the season!

There are many types of seasonal jobs you may not have even considered. H&R Block will teach you how to prepare tax returns and you can be very busy for four months a year (January through April). Or, if you’re in terrific physical shape, you can go work on a crab boat or lobster boat during fishing season. Do you enjoy casinos? You could be a dealer or pit boss during vacation season. Seasonal employment offers many options you have likely never considered.

Next, let’s consider being in your own business. Forget making any big investment as that is not required.

I have covered several specific ideas for starting retirement businesses with no capital in earlier posts. Let me just summarize to say that these businesses can be done part-time or full-time and do not require any special education or skills. Additionally, you have the opportunity of operating an Internet-based business.

On the Internet, you can sell items on eBay or Etsy or Shopify and never leave your house. You can start a blog and earn money by selling advertising on that blog (no need to actually sell anything as automated services take care of getting you the advertisers). You can pick a product that you really love and sell it on Amazon. Or if you write, sell your writing on Amazon.

There are plenty of online courses that teach you how to become an Internet entrepreneur. While you should not plan to become wealthy, you can readily generate sufficient income to retire from a regular job.

The narrow minded perception of retirement, of going cold-turkey from working, is outdated. Very few people can afford a "traditional retirement" and live the lifestyle they enjoy. We know statistically that a minority of people of retirement age have sufficient retirement resources to live off their savings.

So next time you see an article about saving more for retirement, you’ll know that is a single-minded way to think about retirement and a method that has not worked for most. There is no "retirement crisis," there is only an "innovative thinking about retirement" crisis.

You do not need special talents, skills, computer knowledge, etc. We show you multiple ways others are working a few hours a week to generate a comfortable retirement income.

Leave a Reply