Solutions for a comfortable retirement are unfortunately shrinking. This post will highlight some of these disintegrating opportunities and show you how to buck the trend. After we look at the challenges for retirees, we cover some retirement solutions that can still deliver golden years.

Disturbing Trends

Goodbye to Pensions

Pensions (defined benefit plans), as we know them in America, are quickly disappearing and this destroys retirement solutions for many. Private companies have frozen 37% of defined benefit plans, either closing them to new employees or freezing accruals entirely, according to U.S. Bureau of Labor Statistics data.

More pension plans offered by companies will cease or terminate in the next few years. The big problem is that many pension plans are underfunded, over $1 trillion in aggregate. If companies and municipalities cannot meet these future obligations, the impact is a reduction in pension payments to those already retired.

If you are working, the pension plan is likely to cease, and your balance will be rolled over into a 401k -- meaning that any future contributions to your retirement plan will come from you, not the company. If you are already retired, it's likely you will get a lump sum payout as the employer will terminate the plan. In other words—you're on your own. Start with the retirement income calculator to determine your needs to develop your retirement solutions.

When it comes to retirement solutions, you must fend for yourself. Companies, being for-profit entities, are faced with closing down their pension plans because they cannot afford them.

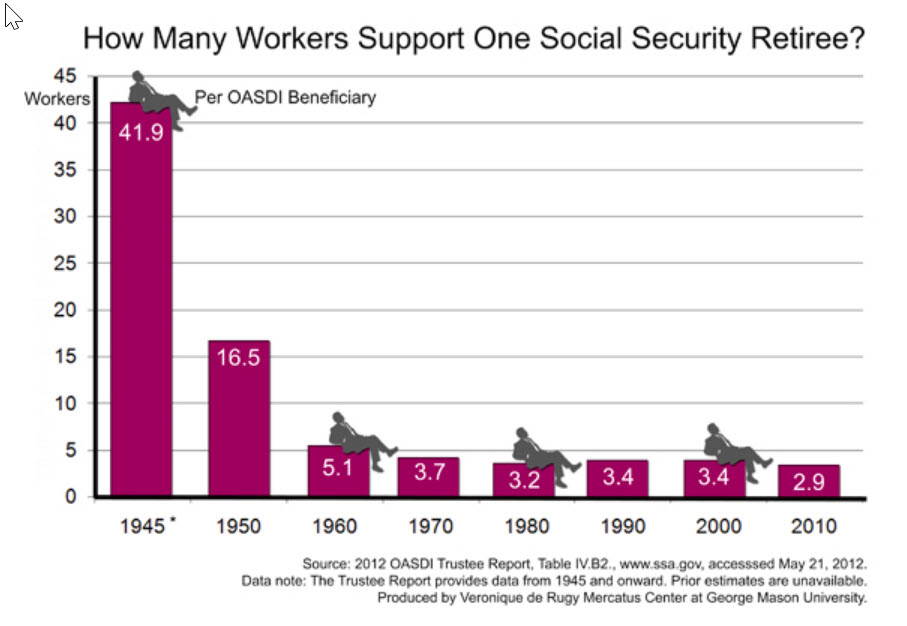

Social Security / Medicare On the Path to Bankruptcy

The US Government can delay facing the music and keep people in denial that the Social Security system will fail.

The US Government can delay facing the music and keep people in denial that the Social Security system will fail.

While people currently age 65 or older will hopefully not see any changes to their Social Security benefits, they will likely see a dilution in their employer retirement benefits, possibly with a reduction in monthly pension payments or the reduction or elimination of health care benefits. Those under age 65 should not rely on anyone but themselves for retirement solutions.

The Social Security Trust Funds are projected to become insolvent in 2034. The Medicare Trust fund reaches insolvency in 2026.

In 2034, revenues coming into Social Security will be insufficient to cover scheduled benefits, causing all beneficiaries to suffer a 23 percent benefit cut, regardless of their age, income level, or how much they depend on the program.

While you may think Social Security insolvency can be fixed by Congress, it cannot be remedied unless you want to place a financial yoke on your children and grandchildren. While you may think that social security payments you receive come from your account to which you deposited, that is false. Part of every retiree's social security check comes from taxes of those now working.

The problem is that the number of retirees is increasing and the number of people working is shrinking.

The problem with Social Security is not Congress, and there is no one to blame. It is simply the aging of America which makes the burden too great for workers to bear.

Poor Budgeting

When I was a financial advisor years ago, I created a portfolio for a retired couple. Combined with their Social Security and the investments, they would have $80,000 per year of income. That may sound like a lot, but they live in Northern California where the cost of living is high.

I issued a checkbook to them so that they could tap the dividends and interest being generated by the portfolio. When I glanced at their activity, I noticed some large checks that seemed inconsistent with the agreed upon budget.

I learned that the wife was visiting her sick brother 3000 miles away with no regard to the cost. Against my warnings, the wife continued to spend more than the amount we had budgeted. It did not require any guesswork to see that this couple was heading toward financial insolvency.

It appears that many retirees have a problem creating or adhering to a budget. There has been more than a twofold increase in the rate at which older Americans file for bankruptcy protection and almost fivefold jump in the percentage of older persons in the bankruptcy system.

I am certain that many of these people lived below the poverty line much of their lives and had no other recourse than bankruptcy. I am also sure that others simply spent more than they had.

I was in awe of my mother who lived 15 years in retirement on $20,000 per year. Most of that time, she lived in Northern California, an expensive area. She lived frugally but comfortably.

She lived on her Social Security check in the interest earned from $200,000 of investments. She proved to me it is possible to live on a very small income. Other retirees need to follow this example and reduce their expenditures. This action is top-ranked of all retirement solutions.

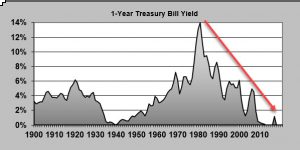

Lower Interest Rates

Retirees are the group most dependent on interest rates for the sufficiency of their income. Until recently, interest rates have been in a 30-year decline.

Retirees who have relied on bank certificates of deposit and treasury securities have suffered. Others who have hired financial advisors or learned to invest have grown their net worth in the equities market. They have also learned how to maintain higher interest income from alternative investments.

Retirement Solutions in Your Control

Fortunately, there is a lot you can control that determines your comfort in retirement. These retirement solutions include:

Where you live—if you live in a high costs area (e.g., New York, California), move to a lower cost area. You may not like this option, but it could be the keystone to your retirement solution program. Lower housing costs mean more that you add to your retirement nest egg.

As an example, I live in California where the price of real estate has created large equity for many. I can sell my home and buy a comparable house using only my equity almost anywhere in the US. I would eliminate my mortgage payment.

The income you need to afford the average home in each state varies from $40,000 to $138,000. The amount also varies tremendously within each state. So choose your retirement location wisely. Also, factor in the total housing cost your property tax and income tax savings.

Your housing expense may be the largest expenditure in your budget. Since reducing expenditures is ranked #1 for retirement solutions, reducing your housing costs takes center stage.

Lifestyle choices

Opt for savings and not luxuries—vacations, luxury cars, dining out, even driving 75 on the freeway instead of 55 all take money out of your pocket today that could go to retirement savings.

I drive a 10-year-old car. I will likely have it for another ten years. Although I could afford to get the latest model every two years, such choices would be foolish for my retirement planning. What financial habits do you have that are wasteful or unnecessary?

When you Retire

Some studies have linked working past retirement with better health and longevity. It has long been known that an important factor of longevity is social interaction. What can keep you involved socially better than going to work? The other impact is on cognitive skills: use it or lose it. Keeping your brain active is the best way to keep decreasing cognitive ability at bay.

Keep working—you may still retire from your current job at retirement age but consider doing what you enjoy and also making money. You can get a HUGE impact on your retirement solutions by working more years (you get the double benefit of not consuming any of your retirement nest egg and having it continue to grow for each year you continue to work).

Work part-time

Finding part-time work with flexible hours is easier than ever. The gig-economy allows you to find work without having specific skills (e.g., Uber). Most importantly, the extra income may preclude the need to touch your retirement capital and provide more flexible retirement solutions. Alternatively, the extra income could allow you to start Social Security benefits later. The later you start, the more you get (up to age 70).

Two other factors make part-time work easier to find. The service sector of the economy is growing faster. These jobs usually do not have high pay, but they also do not require special skills. The demand for labor exceeds supply for these positions. Secondly, companies prefer part-time labor as such workers typically do not receive benefits.

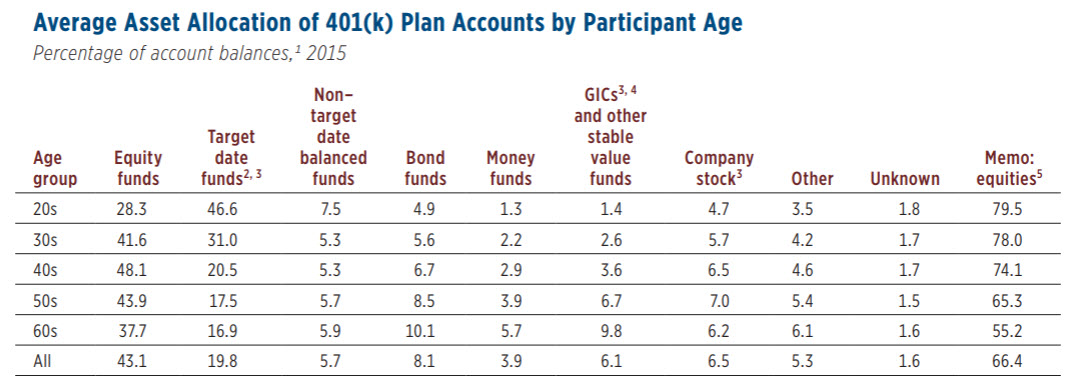

Invest Better

It's easy to let money sit rather than be properly invested. As you see from the table below, investors expose half of their 401k assets to equities, and this should be higher, particularly for those more than ten years from retirement.

Even if already retired, the data shows that keeping at least 50% of your money in equities helps you from running out of money. Moreover, dividends from blue chip stocks have proven to be the best inflation-adjusted source of income over the decades.

Of all retirement solutions, changing the allocation of your investments is easiest.

Mutual Fund Systematic Withdrawal

Say you have a mutual fund with $100,000. On average, it has earned 8% annually. Most of that earnings have been through capital appreciation. In years when the market is up, your fund is up and vice versa. You can have your mutual fund company send you $8,000 annually as a fixed amount.

In theory, the $8,000 is equal to the average 8% earnings and your $100,000 balance should remain stable. In practice, that will not happen. Your outcome will depend on the variation in annual returns.

If the next two years are bad and the fund falls by 10% each year, here are the results:

| Starting balance | $100,000 | ||

| 1st-year change in value | -10,000 | ||

| 1st-year withdrawal | -8,000 | ||

| 2nd-year change in value | -10,000 | ||

| 2nd-year withdrawal | -8,000 | ||

| Starting value year 3 | $ 64,000 | ||

Your results are very sensitive to change in the fund value in the early years after you begin systematic withdrawals. If the early years are positive with big gains, then your fund value will easily withstand later losses. How can you be certain of receiving the same amount annually, indefinitely?

Annuitize

Annuitization means to withdraw from the principal as an income source. Determine how much of your assets you are willing to "annuitize." Some retirees are fixated on leaving an inheritance or a house to their heirs. If they annuitize that asset into an income stream, they can live more comfortably. Annuitization can be accomplished with or without commercial annuities.

If you use commercial annuities, the issuing insurance company guarantees a lifetime income. It's like a second social security check in that it is income you cannot outlive.

For example, in August 2018, a male age 70 investing $100,000 will get $606 monthly for life. The $100,000 cannot be recovered. In return, the insurance company guarantees the income for life.

Tip: the greater the age at which you start lifetime annuity payments, the larger the check you receive. Also, investing in an immediate annuity when rates are high, lock in the benefit of a larger check for life.

Ordering

Ordering is a simple concept. By withdrawing money from accounts where you pay the least tax, you have more money to spend. Thefeore accounts like IRAs, 401ks, and annuities should be the last accounts from which you withdraw (the exception is annuitization of an annuity). Even retirees with modest savings can increase their spendable income significantly be paying less tax with ordering.

Reduce Risk

Of all retirement, solutions are attending to risks such as ill-health and property destruction.

Call your insurance agent today. Is your homeowner's insurance up to date? Would your coverage completely rebuild your home? Do you need flood insurance?

As to health insurance, retirees have it better than pre-retirees. I currently pay $1042 monthly for my wife's (age 64) health insurance. Next year, when she gets covered by Medicare, the cost will drop to $98 per month for her Medicare Advantage plan.

Remember that your health insurance does not pay for long-term care (except in very few situations). So you need a plan for when your health fails. Can a family member care for you? Can you afford in-home care? Should you buy long-term care insurance?

Which of the above retirement solutions have you overlooked? Which can you use for a more comfortable retirement?

Many employers have been shifting from DB to DC plans because they're less costly and provide more investment choices for participants. Unfortunately many people don't manage their 401k plans correctly and find themselves without the needed income at retirement.

Companies want to put the retirement burden on employers. Most pensions are under funded and the rates they return are not high enough so companies know they will have to come up with alot of money. That is why most will stop the plans and make people control thier own money.

Best etf funds lists last blog post..Bond etf.