Learn how CD-type annuities compensate for the failing that many investors perceive with fixed annuities.

Fixed annuities are popular among retirees and senior citizens. The investment is guaranteed, earnings during the accumulation period are not taxed, and annuity payments during the annuitization phase are partially tax-free and can be guaranteed for life. What's not to like?

But some people are unwilling to invest in a fixed annuity because traditional fixed annuities don't provide any interest guarantee after the first 12 months of the accumulation phase. After the initial period of 12 months, the annuity payments could fluctuate and increase or decrease with every passing calendar year.

Of course, once you annuitize (start taking payments) you will have regular annuity payments for the entire duration of the contract. but we still have the issue of fluctuating rates during the accumulation phase. The solution is CD-type annuities.

CD-type annuities (also called multi-year guarantee annuities) offer a fixed interest rate during the accumulation phase - the years when your principal is growing. CD-type annuities are typically offered in terms for 3 to 10 years. Don't be surprised of agents have not mentioned these as the agent commissions are usually lowest on a CD-type annuity.

Sample CD-Type Annuity rates offered as of February 2017:

| CD Type Annuities Representative Rates February 2017 |

|

| Term (years) | Interest Rate |

| 10 | 3.4% |

| 9 | 3.2 |

| 8 | 3.1 |

| 7 | 3.3 |

| 5 | 3.15 |

| 3 | 2.1 |

I recall that I touted cd-type annuities heavily to my clients in 1995 paying 7%, fixed for 8 years. As interest rates declined year after year, I was a hero to my clients for making this recommendation. Of course, I did not earn as much as other financial advisors who sold less favorable annuities (for the client) but paid a bigger commission.

Pros and Cons of CD-Type Annuities

If interest rates remain as hey are for several years or decline, then you will be happy to have locked in a fixed rate for many years. If however rates increase, then you will be locked into a low rate. You can get your funds out as explained in the "liquidity" section below. No one whether interest rates will rise or fall so many smart investors simply build an annuity ladder.

So instead of investing say, $100,000 into a single annuity, you create your ladder as follows:

| CD Type Annuities Representative Rates February 2017 |

||

| Term (years) | Amount | Interest Rate |

| 10 | $20,000 | 3.4% |

| 9 | $20,000 | 3.2 |

| 7 | $20,000 | 3.3 |

| 5 | $20,000 | 3.15 |

| 3 | $20,000 | 2.1 |

You invest $20,000 in five different terms. Then if interest rates rise, the shorter-term annuities will come due and you can reinvest at higher rates. If rates drop, you will have some of your money already locked in at higher rates for several years

The Value of Tax Deferral

In addition to CD-type annuities paying more than bank CDs of a similar term, the interest is taxed deferred. At first you may think,"If it's tax deferred, I need to pay the tax eventually so why bother with the deferral?" You miss the benefit of keeping the tax money and allowing it to compound to give you a larger balance. And income from a larger balance means more income. Let's take a look.

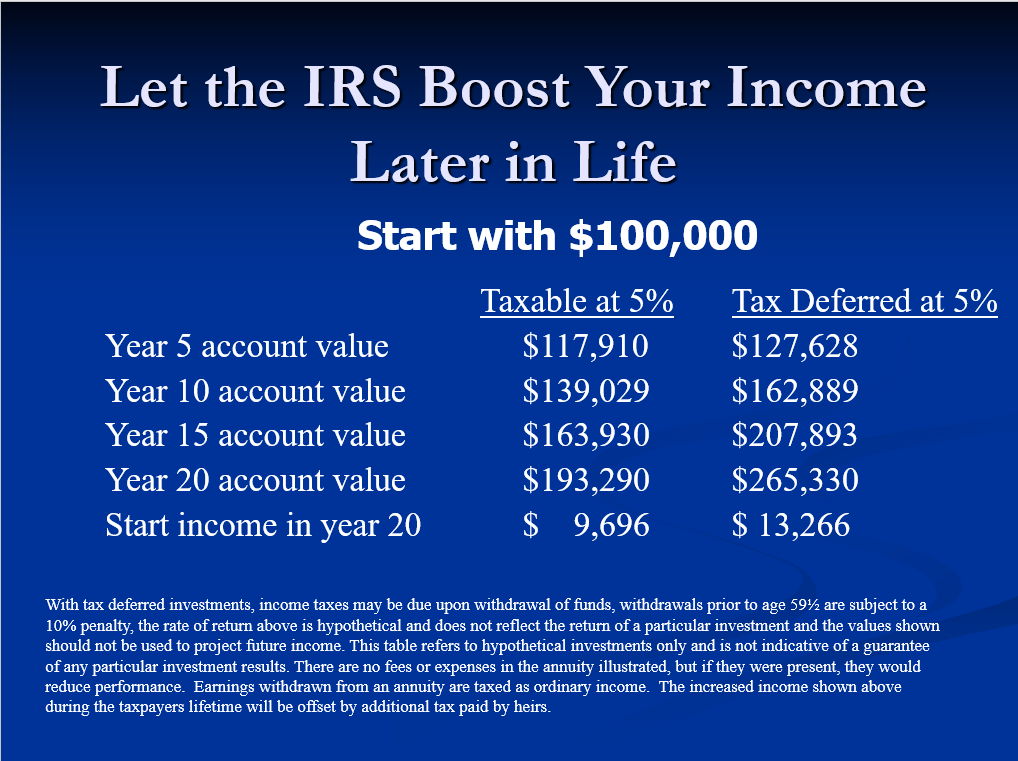

The table below shows money growing at 5%. The left column shows that in 20 years, $100,000 grows to $193,290. The right column, where no tax is paid on the tax-deferred annuity, has an ending balance of $265,330. Which would you rather have -- $193,290 or $265,330? Even though you will eventually need to pay the tax to IRS, in the meantime, the larger balance provided you an additional $3500 of income annually. That's enough for an additional nice trip - every year.

Options for CD-Type Annuities at End of Term

When the annuity term concludes, you will be offered a 30-day period to select your option which is usually:

- renew the annuity for the same term at the prevailing rate (could be higher or lower than the original annuity interest rate)

- annuitize (take annuity payments over a set number of years or lifetime)

- leave the CD-type annuity as an open contract (you can do whatever you want at any time) at a very low rate

- move your funds another annuity company and keep all of your accumulated income tax deferred

- cash in the annuity and pay the tax on all of the income accumulated (the worst alternative unless you need the money very badly)

Like all other conventional annuities, the earnings usually are not subject to income tax while the earnings remain in the account. Additionally, if you move your funds to another annuity company, such transfer when done correctly, is a non-taxable event. Therefore, before deciding to take annuity payments or any other options when your CD-type annuity matures, use the time to shop around and make the choice which best fits your needs.

Safety of CD-Type Annuities

The insurance industry began calling these multi-year guarantee annuities "CD type" annuities as they have a fixed rate for the entire term just as bank certificates of deposit (CDs). Of course, money in banks, up to certain limits, have a federal guarantee. That guarantee does not extend to annuities. Does that mean you take a risk?

There is not much risk in fixed annuities. Your risk is that the insurance company will not be able to pay interest or return your principal. To guard against that, only buy annuities from insurance companies with at least an A rating from Standard and Poor's.

However, even annuities from companies with less than an A rating have not faced much risk. The risk of an insurance company failing is mitigated by the State guaranty funds that exist to bail out failed insurance companies. How the State guaranty funds operate differ from state to state. Some are well-funded, others are not. Some only offer a guarantee up to $100,000 of funds.

But another safety net has come to for in recent years. In the few insurance company failures that occurred in the 1980s, the state department of insurance had the stronger insurance companies take over these failing companies. In that case, the annuity holders did not lose any money. However, their annuity terms were extended and the investors had less liquidity than under their original contracts.

As a practical matter, my advice stands to invest with insurance companies rated A or better and sleep soundly at night.

Liquidity

What if you need your money before the end of the term? When you buy an annuity, you will get a contract which you have 30 days to review. Check the provision in the contract about withdrawals. Some CD type annuities do not allow any withdrawals without payment of a surrender fee. Others allow you to take your interest annually and others allow you to take up to 15% of your balance annually. Each company has different provisions.

It's best that you only invest money that you know for certain you will not need during the term. Use your other funds for liquidity.

Surrender fees

You want to avoid surrender fees as they are expensive, They are the same as the early withdrawal penalty charged by banks. Here is a sample surrender fee schedule for a 10-year CD-type annuity:

| Surrender Charge % | 9 | 8 | 5 | 5 | 5 | 5 | 4 | 3 | 2 | 1 |

| Year | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

Let's say this annuity allows you to remove 10% of your principal in any year without a surrender fee. Let's say that you have 5 years left and your $100,000 annuity has grown in value to $118,195 and you need the cash. The first 10% you take without penalty = $11,819. The remaining $106,375 you withdraw is subject to a 5% penalty in year 5 = $5,319 - OUCH!

And that is why you only invest in a fixed annuity for a term that is comfortable for you and you make sure you have liquidity from other sources should you need it.

Who Should Buy CD Type Annuities?

Generally, people age 55+ are the prime buyers of these conservative investments. I say these are conservative because

- your principal is guaranteed by the issuing insurance company

- your interest rate is fixed and known in advance

- you know the exact date when your funds will be available

Because of these conservative features, CD type annuities are typically used as a tool to create a retirement nest egg or as a savings option during retirement for money that is not currently needed.

Younger people are typically not attracted to such conservative investments. Should they purchase a CD-type annuity, there are federal penalties for withdrawal before age 591/2. The penalty is 10% of the amount withdrawn. There are two ways to avoid this penalty:

- Distributions from a non-qualified annuity before age 59 ½ may be excepted from a penalty when they are paid under an immediate annuity contract. An immediate annuity is defined per IRC Section 72(u)(4) as purchased with a single premium or annuity consideration and the annuity payments start within one year of the annuity purchase. This likely will not help many people as they need to realize within 12 months of purchase that they need money from the annuity and must then annuitize that annuity.

- Another exemption to this penalty is provided by Section 72(q) of the Internal Revenue Code. The exception requires that substantially equal periodic payments be taken from the account for a minimum of five years, or until attainment of age 59 ½, whichever term of years is longer. This is the same rule as applies to those who withdraw money from their IRA before 59 ½.

“CD Type” Annuity Rates

- If you want to keep informed of CD-type annuity rates, here are your sources on the web.

- http://www.annuityadvantage.com/annuitydata.htm

- http://datafeeds.annuityratewatch.com/alliance/app/cd-spreadsheet.htm

- http://www.sfgannuity.com/files/MYG.pdf

It seems like a good marketing ploy to entice someone, who is not already wealthy, that by following what the wealthy do is a good idea for the not so wealthy. First though, what is the tipping point of being 'wealthy' vs not yet quite wealthy enough to be classified as wealthy ? If a person has become wealthy due to a good business or having a good education to have a great job for years, and just saved it away, maybe wealthy NOW and just wants to preserve principal and have safe and steady income from those years of good income and saving of one kind or another. They might not have to worry that the steady income would ever run out in their remaining lifetime. But, for those who do not think they have enough money yet to retire with the 'sleep well at night' notion of a safe but fixed income, that will not run out, off of some 'fixed' quantity of principal, that will not increase since no longer working, handing over a lifetime of accumulation is scary to say the least. Part of the fear of running out of money in retirement is not only the unknown of inflation, but the also unknown of health issues and costs. I think there is a lot more to 'doing what the wealthy do' than just putting all your eggs in the one basket of an annuity. So, although you are trying to make a sale ( with commission ) I question the fiduciary aspect of copying this one part of what the wealthy are doing with only some of their assets. Again, I know you are after a sale, but I am curious of how you can defend your position concerning my arguments and look forward to your reply. [email protected]