How to know when to start Social Security Security Benefits

Here's what the Social Security Administration tells you:

"At Social Security, we're often asked, 'What is the best age to begin receiving retirement benefits?' The answer is that there is no one 'best age' for everybody and, ultimately, it's your option."

This is not the best advice. It could matter when you start payments in making the most of your benefits .

That info, that it does not really matter when you begin social security benefits, is indeed true under the following narrow circumstances:

Most people think that they get the largest payment automatically. Not true. You need to make choices when you apply and if you make the incorrect choice, you get a smaller check -- for life. Even if you already receive Social Security Benefits, you may be able to change your selections.

a) If your individual discount rate for your investments is 5% yearly and

b) you live exactly to your estimated life expectancy and then die.

If the above two presumptions are true, it does not matter when you begin SS benefits, all other elements being equivalent, as the worth of the funds as measured in today's value, is the same. Nonetheless, these two previous assumptions may not apply to you.

There is a method to make a much more informed selection and we'll explain it to you.

In case you are healthier than average and feel you'll live longer than the average person, then it pays to wait longer to begin social security benefits (the opposite is true in case you are in ill heath). Once you consider this issue of longevity, bear in mind that numerous Americans at age 62 are severely overweight, don't workout, have poor diets and have hypertension. In the event you still play tennis three times weekly and are the proper weight for your size, then you're likely going to outlive "average." Ask your doctor about this.

In addition, if your discount rate is higher (e.g. you feel you can earn say eight percent yearly on your cash simply because you're a more active investor), then it pays to begin taking Social Security benefits sooner and put the money to work in your investment portfolio (the opposite is accurate if you feel you are able to only earn say 2% on your funds).

Let's think about this example:

You were born in 1949 and just turned age 62 in 2011. Your full retirement age is 66 (social security income table). Let's imagine you are projected to receive $1,000 monthly in SS benefits at age 66, (depending on your earnings background). Nonetheless, you might begin your SS income now at age 62 and obtain $750 monthly (twenty five percent reduction from your full retirement age amount of $1,000). So do you wait and get $1,000 per month at age 66 or take $750 now at age 62? Or even better, do you wait around to start social security benefits to age 70 and get $1320 per month?

Assuming that your individual 'discount rate' for funds is hypothetically 5 percent (the amount you feel you are able to earn on your money) and that you view yourself as having average life expectancy, you would come out about the same regardless of when you begin payments. (This calculation can be carried out utilizing any financial calculator or spreadsheet with a present value function and the above assumptions.)

Present Value of One's Social Security benefits:

Starting Age Present Value of Payments

62 $124,794

66 $125,905

70 $123,124

Thus, the amounts are practically identical.

However, let's consider a healthy individual with "good family genes." At age 62, average life expectancy is 23.5 years, or age 85.5. But let's assume you feel you'll live five years longer than average (Do keep in mind that the average additional life expectancy of 23.5 years is AVERAGE meaning that 50% of the people live long and 50% don't make it this long). Let's also assume that you are not a good investor and tend to place your funds in bank CDs which only earn you 2%. Now the figures look like this:

Starting Age Present Value of Benefits

62 $195,718

66 $223,476

70 $248,184

For these assumptions, we see that it's worth $50,000 more to wait to age 70 collect SS benefits. Of course, there are other factors which come into play such as if

- you still have earned income at age 62 and how much,

- the pattern of your income through your retirement years (e.g. are you getting deferred compensation until age 65, which impacts your tax bracket making it more beneficial to put off you SS benefit commencement date)

- the amount of your SS benefits which are subject to tax and that is influenced by the amount of your other income

In the future posts, we will address other concerns like increasing Social Security benefits for those who are married and those who are widows or widowers.

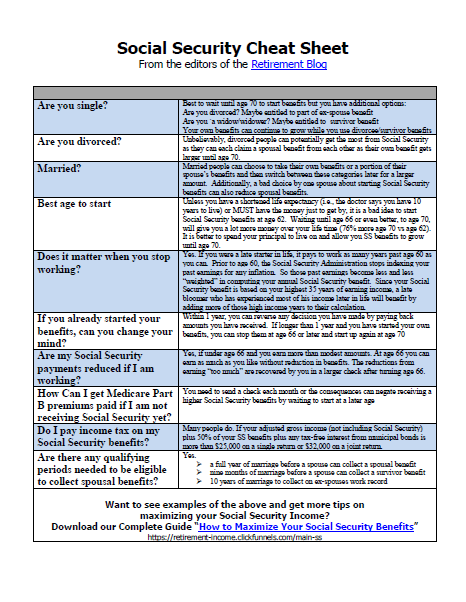

Maximize Your Social Security Income

Get the one-page social security Cheat Sheet

You may think that the folks at the Social Security office will tell you how to get the biggest monthly check. In fact, the federal rules PREVENT them from advising you. There are millions of people who have given up more than $50,000 just by making a simple yet incorrect method of taking their Social Security benefits. Don’t let that be you! Get your free copy now.

"At Social Security, we’re often asked, “What is the best age to begin receiving retirement benefits?” The answer is that there is no one “best age” for everybody and, ultimately, it’s your option."

In other words, You are paying our salaries, but we we're still not going to give you financial advice. Ah, the ol' bureaucracy!

honest question... will social security even be around with all this crazy stuff going on? Do not want to be mr. negative here but...

Spouses are entitled to a Social Security payout of up to 50% of the higher earner's check (if that amount is higher than benefits based on his or her own working record). Retired couples in which one spouse didn't work or had low earnings have the most to gain from this provision.

Good information, thanks. I'm just concerned about the future of Social Security. We will see.

With 10,000 people reaching age 65 every day, the whole country is thinking more about social security. I'm of a mixed mind. If I can $50,000 more by waiting, but I have to continue working ...

I think that that social security will have to continue to be modified to accomodate the growing number of recipients and our ballooning deficit. Unless you are nearing retirement age there is not much point in even calculating the benefits.

honest question… will social security even be around with all this crazy stuff going on? Do not want to be mr. negative here but…

social security is defiantly a growing concern its something that needs to be handled correctly as its a need for all americans

This is very important. More than half of all retirees depend on social security as their main source of income. So they'll need a good way to get as much benefits as possible.

i am 63, fairly active and in good health and i live outside of the usa so i am eligible to make a fair amt each year free of us taxes [however i do pay taxes where i presently live]. i assume i may be able to continue to do this after retirement? i still work now and like it so i suppose i could still work until i feel like quitting and not be penalized as would someone working and drawing soc sec in the usa?

Maximizing Social Security benefits short-term is great, but there's such a huge long-term problem. There simply isn't enough money as things stand now to keep Social Security afloat in its current state. I'm concerned that the retirement funds I've been counting on aren't going to be there. I've been reading articles by Peter Orszag and he points out many of the problems and possible fixes. orszag.net I know there are other great minds out there with good ideas. Hopefully someone comes up with something soon.

Social security income is an increasing concept nowadays. Any one can start this at any age...Thanks...nice post.

Good information, thanks. I’m just concerned about the future of Social Security. We will see.

social security is important for the retiree ...

Social Security has been an ongoing concern for me as I am not getting any younger! This article has given me some great insight into this and good guidance. Thanks

Thank for your article.

But I have a lot of questions about this problem: Is the time of a new Social Security´s Model? A high percentage of Foreigner countries have it, here....why not?

full retirement age rise and average life term rise also...social security will have to continue to be modified to accomodate the growing number of recipients and our ballooning deficit.

Unfortunately, I don't think social security will even be around when I'm old enough to collect.

In case you are healthier than average and feel you’ll live longer than the average person, then it pays to wait longer to begin social security benefits (the opposite is true in case you are in ill heath. I am 54 now and blessed with good health. Hope I will be at 62 but no one knows what the future holds.

Thanks for the nice article on social security,Great Read

The above calculation show that the older you retire the Social Security benefits you collect. In my opinion it is best not to depend on the government for your retirement as the government could cut their benefits anytime.

I am going to start my own business to fund my retirement.

Nice tips. Unfortunally we have no such retirement plans. I wish someday we will have one. Anyway keep going to share your knowledge. Thx u

Social Security planning is so important. I'm about 30 and I think about this and factor it into my financial planning. However, I don't even know if it will be there or not.

It's not always as straight forward as this article makes it out to be, but it is at least a good start.

Every few years, I get a letter from social security stating that social security benefits may not be there in full when I reach retirement. I hope they get it sorted out.

At first glance I thought that it would be wiser to wait until you reach 70 to claim your benefits but isn't it that at the age of 70 you cannot use it as much as you can when you are just 60? I mean 60 is a great age to enjoy life and all your earnings. 70 may be the time to enjoy life at home. 🙂

i think there are lots of benefits from social security and if we can utilize it property we are definitely going to reap greater rewards in the future..