I offer an analogy to explain social security cash flow.

I offer an analogy to explain social security cash flow.

Suppose that you had two pockets.

Each Friday you get paid and put your money in your left pocket.

For any money you need to spend, you take it from your right pocket.

Most people think that they get the largest payment automatically. Not true. You need to make choices when you apply and if you make the incorrect choice, you get a smaller check -- for life. Even if you already receive Social Security Benefits, you may be able to change your selections.

Without noticing it, you have been taking more money out of your right pocket than you have been depositing to your left pocket.

When asked you how you are doing financially, you show all of the loot your left pocket (the pocket where you make deposits but never any withdrawals). But really, you are going broke.

How Does Social Security Work?

The left pocket is Social Security. The right pocket is the US Treasury.

The left pocket keeps getting deposits. It gets deposits from two sources:

- From the money taken from the paychecks of your children and grandchildren

(Social Security has already paid out to you and other retirees much of the money you deposited long ago from your paycheck ) - From the interest earned on Treasury Securities that comes from the right pocket

You may remember that the right pocket (the US Treasury) has a problem. It spends more money than it receives. In fact, to pay interest each year to the left pocket, the right pocket has to borrow money. It borrows money from American citizens, the Chinese government, the Japanese government and anyone else who buys treasury securities. These borrowings are required so that the US government can keep the general economy and Social Security afloat.

Would it be okay if we simplified things and just put the money from both pockets into one bucket (both pockets belong to you anyway)?

Social Security Cash Flow

Here’s what we have – a picture of the income and outgo of the Social Security system when viewed as one bucket:

| Income | Outgo | Net Cash FLow | |

| 2006 | 642.5 | 555.4 | 87.1 |

| 2007 | 674.7 | 594.5 | 80.2 |

| 2008 | 689 | 625.1 | 63.9 |

| 2009 | 689.1 | 685.8 | 3.3 |

| 2009 | 689.1 | 685.8 | 3.3 |

| 2010 | 663.6 | 712.5 | -48.9 |

| 2011 | 690.7 | 736.1 | -45.4 |

| 2012 | 731 | 785.8 | -54.8 |

| 2013 | 752.2 | 822.9 | -70.7 |

| 2014 | 786.1 | 859.2 | -73.1 |

| 2015 | 826.8 | 897.1 | -70.3 |

What do you notice about the income and the outgo starting in 2010?

Social Security paid out more than it took in.

Wait a minute. Didn’t you just read on CNN.com that the Social Security Trust Fund will last through 2034?

Yes. The trust fund, a fictional accounting gimmick, will last through 2034 (maybe). But regarding social security cash flow, the Social Security Administration has been paying out more than it takes in for six years. That negative cash flow will continue to grow.

Let’s state this another way. The money you get from Social Security each month is collected from the paychecks of your children and grandchildren. What happened to the money you deposited? It was not sufficient to last your lifetime and has already been paid to you and other retirees. Take a look at this Social Security benefits statement to see this.

Because that amount taken from the paychecks is not sufficient to cover what all of the retirees receive as Social Security Benefits, the US Treasury borrows money to make sure it can make good on all of those Social Security checks.

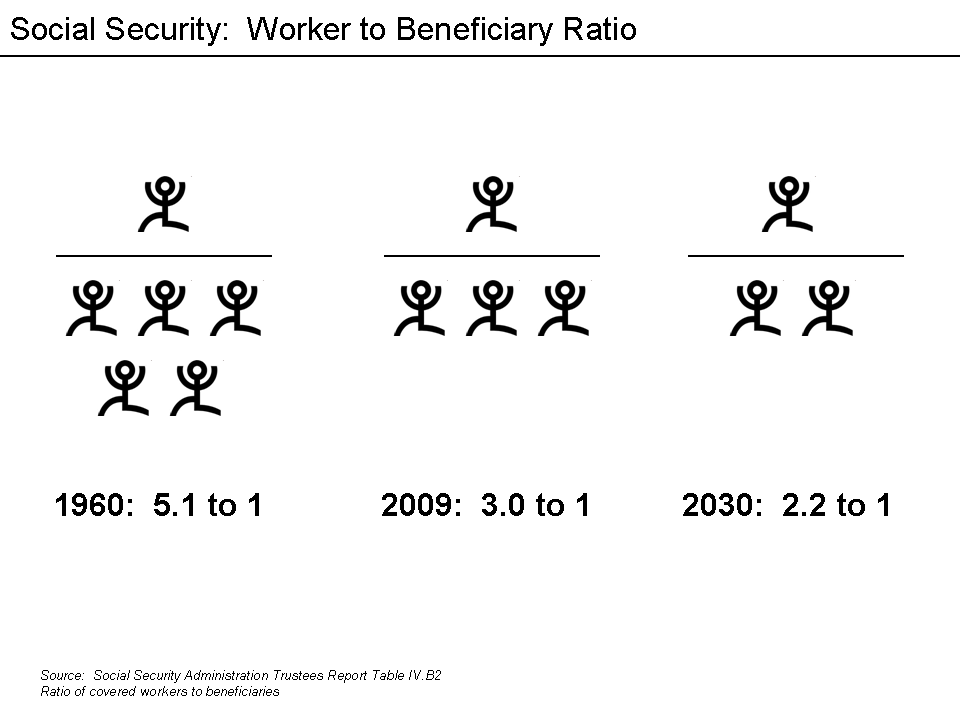

You have likely seen this graphic in the past:

This situation cannot work out well.

I passed the CPA exam when I was 19, so I am a pretty good accountant. You can bet that the above numbers and analysis are accurate. You can bet that this is the most straight-forward and honest look (albeit simplified) you have seen for how Social Security works.

I am not the first one to write on this. The Brookings Institue also published an article about the same observations in 2011.

Please ignore what you hear from AARP, your Congressperson or some other person with political motivation to obscure the facts. The cash flow figures above are from the 2016 OASDI Trustees Report.

It is only when you set aside political agenda and put facts before opinion that you can see the truth and make better decisions. However, if you are like the average American, you will stick to your pre-formed opinions and ignore these facts.

"Once in a while you encounter members of the human species with so much intellectual superiority that they can change their minds effortlessly."

The Black Swan, Nissim Taleb

The Solution to Make Social Security Work

Workable options for the viability of social security cash flow have passed.

In 1981, at the age of 25, I read an analysis by Michael Boskin, then an economics professor at Stanford. He showed that for people of my age, the dollars we placed into social security had a negative return. In plain English: for each dollar taken from my paycheck and deposited into social security, I would get back less than a dollar (the opposite was so for my parents--they got back a LOT MORE than they deposited).

Fortune Magazine published my response to the article which asserted the solution to healing social security cash flow: remove the promise to pay any social security benefits to people, who at that time, were age 40 or younger. These people had plenty of time to prepare for their retirement independently, without reliance on social security benefits. Secondly, keep the promise to everyone age 41 or over and let them collect the promised benefits. In other words, slowly phase out social security because demographics do not support positive social security cash flow.

It is now too late for such a solution to balance social security cash flow. The remaining options are:

- To start benefits to social security recipients at later ages. For example, do not allow people to get benefits at age 62, Make them wait until age 66 or older

- The unconscionable option of increasing the social security tax on your children and grandchildren.

Note that either option will not solve the problem--it will only delay the collapse further into the future.

Given that we have past the time when a viable solution will work, all we can do is wait for the calamity.

You saw a similar situation in 2008 with the great recession. As a society (actually, the politicians you voted for), we permitted financial institutions to make guarantees they could not keep. By the way, your politicians still have not fixed this problem as it is still possible for say AIG, to guarantee the value of securities that far exceeds AIG's ability to pay (they got a bailout to keep them afloat in 2008).

So when a problem is ignored, it eventually does get solved by a calamity.

Maximize Your Social Security Income

Get the one-page social security Cheat Sheet

You may think that the folks at the Social Security office will tell you how to get the biggest monthly check. In fact, the federal rules PREVENT them from advising you. There are millions of people who have given up more than $50,000 just by making a simple yet incorrect method of taking their Social Security benefits. Don’t let that be you! Get your free copy now.

Very interesting I'm glad I ordered it thank you

I started collecting my social security at age 62...due to a death of my fiance'...I now am.not working...and only living on less than $700..amon

I started at 62 and living off 700 a month 400 retirement and 300 supplement. Can I receive more.

Please get a free copy of our booklet on maximizing social security benefits

https://retirementbooklet.com

We as Retirees I’m finding are kinda treated like we are throw-always and useless. I am still a strong individual, coming up on 71. I am an Artist, an advocate for other seniors. I was an Esthetician, and a Licensed CNA until I Retired at the age of 62. I had life changing circumstances. To be told by a Doctor Recently that all Elderly forget!!! I’m now tracking how many times he Remembers things he has done, sometimes it’s easier to forget!

I started drawing at age 62 and only get 783. Dollars a month to live on. I am 73 and still working . My husband did the same and he is 71 and still working as we have to to survive.

This is not true. Congress keeps borrowing from social security for other things. While we all contribute. There is enough coming in to cover the benefits, Congress needs to stop robbing the fund blind. They borrow but they haven’t paid any of it back. That’s the real reason SS is going broke .no one is holding Congress accountable for the SS money they are taking and not paying back. Accountants should know this. They are teaching this in degreed programs through out universities. Maybe it’s time for a refresher course??

The US government borrows continuously through the sales of treasury securities. These securities are sold to social security, to a foreign government and to institutions and individuals. When these securities reach their maturity date, they are paid in full. However, in any year, the government sells more new securities than reach maturity and thus, the US debt continues to grow. The reason that social security is going broker is that it pays out more money than people have contributed. That is the ONLY reason. You can believe whatever fiction you like but on this blog, all statements are based on facts.

Please send details