“When Can I Retire,” is what people ask from several different viewpoints. Commonly they mean:

- when can I retire and collect my Social Security

- when can I retire and get my pension payments from work

- when can I retire and access the money in my 401(k) account

- when can I retire, given my existing financial resources and amounts I can accumulate in the future

I will answer all four of these questions in this post. If you have a different concern about, “when can I retire,” just ask it in the comments box at the end of the post and we will get you an answer.

When Can I Retire and Collect Social Security

When can I retire to get social security benefits?

When can I retire to get social security benefits?

If you’re divorced or your spouse has died, you can start collecting Social Security as early as age 60. For everyone else, the minimum starting age is 62. However, be aware that if you start taking your Social Security benefits at the earliest possible age, you will receive a smaller check than if you wait to start benefits at a later age.

Consider the fact that your starting age determines the size of the check for the rest of your life, this can be a big decision. Your monthly Social Security benefit will grow for cost-of-living adjustments, in other words, inflation. In recent years, these adjustments have been small or nonexistent because the rate of inflation has been very low.

From a purely financial viewpoint, it is best to start at age 70, when your benefit will be as large as possible. This recommendation assumes that you will spend your Social Security benefit and not invest it. In other words, the time value of money for you is zero. Additionally, if you need the money to live, file for benefits at age 62.

The one caveat is if you are still working. Your social security benefit can be reduced.

Social Security Reductions if Working

Here’s how that works. If you are under age 66 for the entire year, social security deducts $1 from your benefit payments for every $2 you earn above the annual limit. For 2017 that limit is $16,920. In the year you reach age 66, social security deducts $1 in benefits for every $3 you earn above a different limit, but they only count earnings before the month you reach your full retirement age. If you will reach full retirement age in 2017, the limit on your earnings for the months before full retirement age is $44,880.

If you know you are close to these above limits, it makes no sense to file for Social Security benefits. But if you unexpectedly earn more, there's good news. The amounts of early retirement benefits you lose as an offset against your earnings are not necessarily gone forever. When you reach full retirement age, Social Security will recalculate upward the amount of your benefits to take into account the amounts you lost because of the earned income rule. The lost amounts will be made up only partially, however, a little bit each year. It will take up to 15 years to completely recoup your lost benefits.

When to Take Social Security--Other Factors

Another factor is your health. Obviously, if you're age 62 and your doctor says that you have eight years to live, start your Social Security benefits today.

Another factor depends on your plan to spend or invest your social security benefit. See the table below. If the interest you earn on the money is zero (i.e. you will spend the money and not invest it), the math argues to delay your benefits until age 70 to get the most.

However, if you plan to invest the money, you see that if you earn 3% annually, at age 85,you have accumulated the same amount whether you start benefits at age 62 with a smaller amount or wait for the larger amount at age 70.

But if you earn 6% or more, then start benefits at age 62 and invest the money. You will always be ahead through age 100.

Here is the summary showing the three different interest rates you will earn on your benefit and the yellow highlighting shows the approximate break-even age between the 3 choices (start benefits at age 62 vs 70). After the break-even year, starting benefits at age 70 provides more life time benefits.

| Assumes 0% annual interest |

Start |

Start |

| monthly payment |

$750 |

$1320 |

| accumulation age 70 |

$72,000 |

0 |

| accumulation age 80 |

$162,000 |

$158,400 |

| accumulation age 85 |

$207,000 |

$237,600 |

| accumulation age 90 |

$252,000 |

$316,800 |

| accumulation age 100 |

$342,000 |

$475,200 |

| Assumes 3% annual interest |

Start |

Start |

| monthly payment |

750 |

1320 |

| accumulation age 70 |

$81,463 |

0 |

| accumulation age 80 |

$214,991 |

$184,919 |

| accumulation age 85 |

$298,343 |

$300,352 |

| accumulation age 90 |

$395,167 |

$434,442 |

| accumulation age 100 |

$638,288 |

$771,135 |

| Assumes 6% annual interest |

Start |

Start |

| monthly payment |

750 |

1320 |

| accumulation age 70 |

$92,582 |

0 |

| accumulation age 80 |

$291,967 |

$217,402 |

| accumulation age 85 |

$446,409 |

$385,800 |

| accumulation age 90 |

$654,728 |

$612,943 |

| accumulation age 100 |

$1,314,735 |

$1,332,589 |

Note that we have not considered income taxes or COLA increases to keep this comparison simple. It is possible those factors could change the your decision and the above analysis.

When Can I Retire and Get My Pension?

The rules for collecting pension vary from company to company and employer to employer. However, they all have a similar structure.

The rules for collecting pension vary from company to company and employer to employer. However, they all have a similar structure.

Typically, there is a minimum age at which you can retire and begin collecting payments. That age is typically 55 but ask the human resources department yourself, "when can I retire?" and let them explain. The amount you receive, say as a monthly check, depends on your age and years of service at the company.

Here's an excerpt from the IBM Pension Plan summary, which is a good example of a typical company pension:

- The normal retirement age is defined as the later of age 65 or the completion of one year of service

- Participants earned points as follows: 0.16 basepoints each year until a 4.25 base point cap was reached, and 0.03 excess points each year until a 0.75 excess point cap was reached.

- The total point value is converted to an annuity at the benefit commencement date based on pre-determined annuity conversion factors.

- A participant may receive his or her benefit immediately following the termination of employment or may defer benefit payments until anytime between early retirement age and normal retirement age.

- Early retirement age is defined as:

- Any age with 30 years of service;

- Age 55 with 15 years of service; or

- Age 62 with five years of service.

- Under the Pension Credit Formula, a participant who terminates employment and whose pension benefit commences before his or her normal retirement age will receive smaller monthly annuity payments than if his or her benefit commences at normal retirement age.

Therefore, you simply need to either read the pension document from your employer or talk with the people in human resources to know the answer to "when can I retire," how much you can receive and how to maximize the amount you receive.

When Can I Retire and Access the Money in My 401(k) ?

Your 401(k) account belongs to you and can be accessed as soon as you leave your employer. However, if you access the 401(k) account and withdraw money prior to age 59 ½, you will pay a 10% penalty on the amount withdrawn. There are exceptions to this early withdrawal penalty explained in separate posts. The general exceptions are:

Your 401(k) account belongs to you and can be accessed as soon as you leave your employer. However, if you access the 401(k) account and withdraw money prior to age 59 ½, you will pay a 10% penalty on the amount withdrawn. There are exceptions to this early withdrawal penalty explained in separate posts. The general exceptions are:

If you are age 59 ½ or more, you are free to withdraw your 401(k) account and spend all the money if you desire (you will owe deferred income tax on the amount withdrawn). Most people rollover their 401(k) account to their own IRA. IRA accounts typically provide much broader investment selections than the typical 401(k) plan.

Whether you leave your money in your employer’s 401(k) plan or rollover to an IRA, you can set either account to pay you a fixed retirement income. This could be a specific dollar amount or percentage of your account per month and thereby have a relatively steady retirement income.

When Can I Retire, Given My Existing Financial Resources

Your own savings are often the major determinant in the concern if when can I retire.

Let me share with you a rule of thumb called the 4% rule that is often criticized. However, I have found that the 4% rule is as good a planning tool as far more sophisticated methods to determine how much you can safely withdraw from your retirement savings.

By the terms “safely withdraw,” I mean how much you can withdrawal per year or per month and not exhaust your assets.

Let’s assume that you have a total of $400,000 of retirement savings. That could be any combination of money in a 401(k), and IRA, stocks, mutual funds or money in the bank. The 4% rule says take 4% of the amount in your account and then add an inflation adjustment each year. For example, in year 14% of 400,000 would be $16,000 to withdrawal. The next year, you would add the rate of inflation, say 2%, and withdraw $16,320. William Bengen, the founder of the 4% rule, concluded that 4% was the highest withdrawal rate you could use to have your savings last 30 or more years.

There have been many financial planners who have analyzed the 4% rule and criticized it. Some are critical that if the market declines for two or three years in a row and your nest egg shrinks, the 4% rule could be too aggressive. Others believe that the 4% rule is to conservative and restricts your living standard. Author Paul grand guard wrote a book indicating how 6% could be a safe withdrawal rate.

The safe withdrawal rate has a lot to do with how your money is invested. Those with more invested in stocks or stock mutual funds, can withdraw more overtime than more conservative investors.

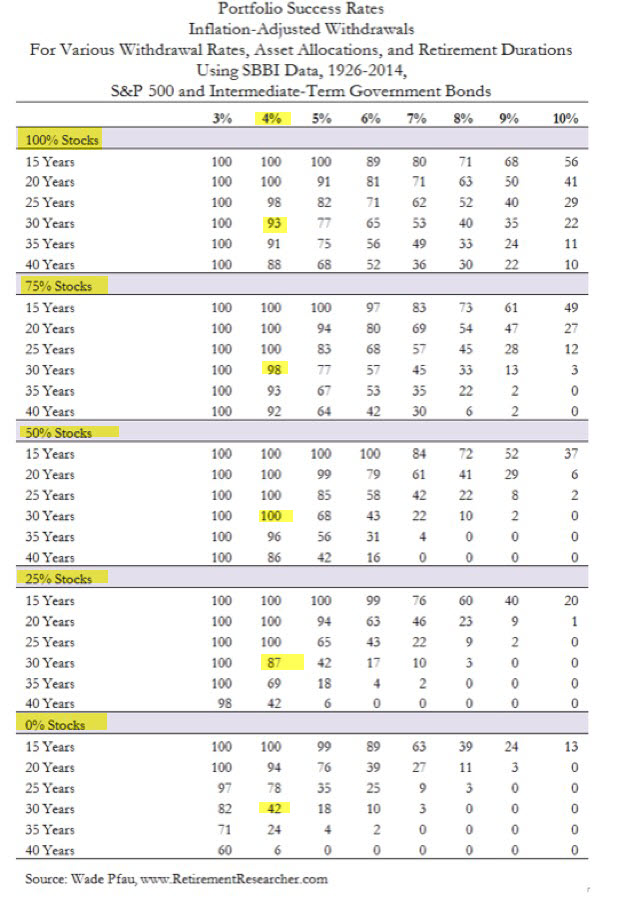

A study which looked at the market from the period 1929 through 2014, found that those who invested more aggressively, i.e. held a higher percentage of stocks, could take larger annual withdrawals. Here is the table:

The table shows that if you withdraw 4% a year of your nest egg, a portfolio of 75% stocks has a 98% chance of lasting for 30 years without exhaustion. But further down the column, we see that a portfolio that has no stocks only has a 42% chance of lasting 30 years without exhaustion

If you bump you withdrawal rate to 5% and look down that column, you see that portfolios with higher concentrations of stock, or stock mutual funds, have a higher probability of lasting 30 years than those portfolios with lesser concentrations of stock. This illustrates an important paradox retirees.

Important Paradox of Retirement Investing

Retirees generally seek a desire for emotional comfort. So they place their funds in “secure” investments such as bank accounts, treasury securities and other fixed income instruments. In fact, we see that the table which depicts the last 85 years shows that such a conservative investor will in fact be less secure. Specifically, there nest egg will run out faster.

The paradox is that those with a modest amount of assets, must continue to allocate a significant portion of their nest egg to the equity markets. It’s only the wealthier, say someone with a nest egg of $3 million, who can invest that money at a low rate of interest and still generate sufficient income to support a modest lifestyle.

Emotional Comfort

Because of retirees' concern about losing money and not being able to make it back again I recommend the bucket method. The bucket method has you divide your money into at least three buckets, say short-term, medium-term and long term

The short-term bucket, might contain certificates of deposit and treasury securities that all mature in the next five years. This bucket gives you the emotional comfort that your spending needs up for the next five years are allocated to investments that are a sure bet.

Your medium-term bucket might contain a mixture of bonds and high dividend stocks (e.g., utilities and REITS) that are able to maintain their dividend even during market declines.

Your long-term bucket contains stocks that you hold for growth of capital. You will not touch this bucket for the next 15 years. Here’s the good news about holding stocks for at least 15 years. In every 15-year period since 1929, stocks have never lost money.

By allocating money in this manner, you don’t get nervous when the stock market declines because you know that you won’t need to rely on that bucket for many years. Let’s say your expectation for that bucket is to grow 8% annually which means it will double in nine years. Should that bucket grow faster than expected and double in less than nine years, you can take off the excess and move it to your more conservative medium or short-term buckets.

The point of the bucket system is to keep you feeling comfortable about how your money is invested and being able to retain a significant portion of your portfolio in stocks. Why? Because we’ve seen from the past, that is significant allocation to stocks make your retirement more secure over the long run.

Very Interesting, Would surely like to have that booklet, I"m turning 62 yrs. in August, and I receive SSDI, What's gonna happen to my Income, Mine you, I still work Part-time, Please help..