Stocks for Retirement Income - Surprising Evidence

An issue that plagues many retirees is how to create retirement income in the face of the increasing cost of living. Even with moderate inflation, costs of living tend to increase over time. This can reduce the income retirees can obtain from fixed income investments, even while they must meet higher expenses. Where can you find a source of retirement income that can keep of with inflation, along with your expenses?

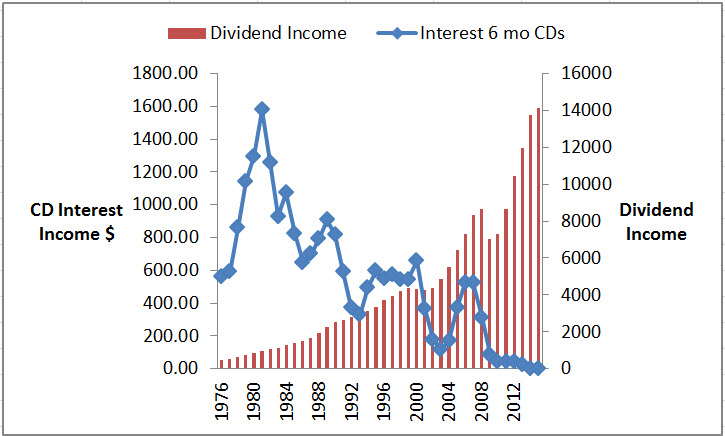

Our suggestion - use stocks for retirement income. Consider putting some of your money into a portfolio of large capitalization dividend-paying stocks as a retirement income generation alternative. This could help to provide you with an income that keeps pace with the rising costs of living. For the 40 years ending 12/31/15, the stream of dividends from an investment in a basket of dividend stocks representing the S&P 500 index generated a growing stream of retirement income. During that same period, interest rate from CDs fell from 6% to .27%.

Data 1/1/76 through 12/31/15. Dividends based on a $10,000 investment 1/1/76 in a basket of stocks representing the S&P500 from American Funds Distributors. Interest rates from Federal Reserve year end rate on 6 month CDs. You cannot invest directly in an index. Past performance is not a guarantee of future results and an analysis of a different period may have revealed different results.

Although publicly traded stock can help you to manage inflationary risks, the dividends that these stocks pay out are highly dependant upon the overall profitability of the issuing company. Therefore, you will want to strongly consider the dividend payment history of the company prior to investing. To secure reliability of stocks for retirement income, you want stocks ranked highly for safety by research services such as Morningstar or Valueline.

While the average retiree would vote for insured CDs as a more secure alternative, the included chart shows that in fact, living on dividend income stocks was a more secure and more sure provider of dividend income as a solution to low interest rates.

A few additional things should be considered about stocks for retirement income and CDs. First publicly-traded stocks tend to be suited for investors that are seeking asset appreciation and are willing to take on the additional investment risk. On the other hand, CD's are suited for investors that are concerned about preserving their principal investment and are adverse to market risk. With this in mind, it should be remembered that CDs are FDIC insured while publicly-traded stocks are not. The values of publicly-traded stocks fluctuate in value and may result in either a gain or loss upon sale.

The income from these investments is also subject to differing income tax rules. Stock dividends are generally subject to federal income tax of 15% (and maybe lower for many retirees), while CD interest is taxed as ordinary federal income tax rates, which can range anywhere from 10-39.6%. CDs may have an early withdrawal penalty if money is taken prior to maturity. On the other hand, the stock of most largely capitalized companies can typically be purchased and sold at any time when the market is open.

Also keep in mind that you can get quick cash against a portfolio of stocks. Brokerage firms will lend money without need for application or credit check against your stock portfolio. The rates on these loans is generally lower than any other borrowing costs. And the funds are available to you anytime simply by writing yourself a check.

If you still feel that stocks for retirement income is risky, please take a look at the findings of the Trinity Study. That study shows that retirees have in fact been more secure by maintaining 50% of their investments in stock.

Leave a Reply