Financial investment firms, more often than not, have been fined and penalized multiple times for ignoring rules, regulations and laws. Yet regulators allow these companies to continue operations and the public continues to do business there. What gives?

“JPMorgan Chase to pay $307 Million for Steering Clients to its Own Products,” reads the NY times headline

I don’t want to single out JPM, but I use them as an example of how the financial services industry treats their clients. It's not pretty and it's not right.

Almost every financial investment firm is likely guilty of same as you will learn in this post: Merrill Lynch, UBS, Nationwide, Prudential, etc. If your brokerage firm or life insurance company offers products with their name on it (usually mutual funds and annuities), know:

One page "invest like the rich" cheat sheet provides short explanations of how the rich investment differently. You don't need to be rich to copy what they do. Download now.

- That financial investment firm is not providing you independent advice

- You are being steered to their own products regardless of relative performance

- You may be paying higher fees

How can this go on and why isn’t the government protecting you?

The reason that financial investment firms can do this is because you allow it. My guess is that more than 50% of the people reading this post have an account with a large financial services firm that markets their own mutual funds and annuities. But will you go and close your account tomorrow now that you see these firms will violate rules, regulations and laws just to profit from you?

If you keep your account open, it is a signal to these financial investment firms that they can get away with this behavior. So you are the culprit.

As to the government protecting you, never depend on that. The government cannot attract the same talent as the financial services industry. The white collar fraudsters at financial investment firms are smarter, went to better schools, have better experience and get paid a LOT more. The enforcers who work at the SEC, the folks trying to protect you, are simply outgunned by the shysters who manage your brokerage firm and insurance company.

(c) Can Stock Photo

It’s important to state that your individual financial advisor or agent is likely a very trustworthy person. I will bet that 99% of the people who work at your financial investment firm are trustworthy and have integrity. It is the 1% at the top, the most senior management, who set the policies and develop schemes to steal your money. Senior managers never look you in the eye and lie to you face to face. It’s easier when they don’t know your name. They take your money in the dead of night without your realization or permission.

About the JP Morgan $307 million fine, “The undisclosed conflicts were pervasive” said Andrewe J. Creseney, head of enforcement at the SEC.

“Conflicts” means “conflict of interest.” It is totally legal for your financial investment firm and insurance company to act against your best interest. However, when the managers at the company set policy to do so, they must disclose it. In this case, JPM did not disclose that client funds were being pushed into their own products: proprietary mutual funds. In other words, the firm made it a policy, when it had the ability, to place client money into their own higher-expense and potentially worse-performing funds. This is legal as long as they tell you.

The failure to disclose this is actually quite dumb. Management could have handed out a 70-page document with one page making the necessary disclosure and the other pages comprising filler. No one would have read the document and JPM would not have been fined $307 million.

(It is surprising that these white collar crooks get caught so often. Lack of disclosure is a frequent issue for which financial investment firms are fined. This is easily remedied by making very long and lengthy disclosures which no one will read. Haven’t they figured that out)?

By the way, you should not feel singled out if you realize you've been sold a fund with a name like “JP Morgan Chase Bond Fund” or the “Merrill Lynch Growth Equity Fund” or “The Nationwide Balanced Income Fund” or some other name which indicates that you own a high-fee proprietary fund of your financial investment firm.

You have done no worse investing than the people in this TV ad:

Be comforted in knowing lots of other people have lost money for many other reasons as these headlines below indicate.

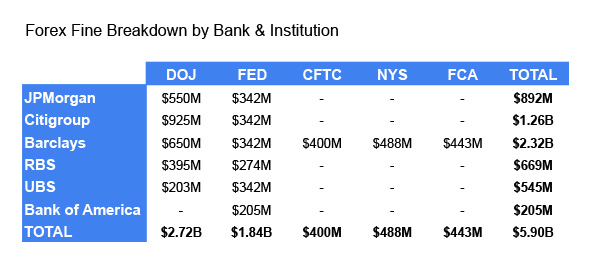

Rigged trading of the U.S. dollar and the euro

JPMorgan, Citigroup, Barclays (BCS), and Royal Bank of Scotland (RBS - Get Report), will pay $2.5 billion and plead guilty to violating antitrust laws. Here are the fine amounts below levied against each firm (firm names in the left column, government agency collecting the fines in the first row, amounts in millions of dollars). Do you do business with any of these financial institutions?

Other fines against JPM for customer disregard/intentional gouging:

Credit Card Borrowers - $136,000,000

JPMorgan Chase will pay $136 million in penalties to the Consumer Financial Protection Bureau and states to settle charges that it used illegal tactics to target delinquent credit card borrowers.

Armed services members - $35,000,000

In April 2011, JPMC agreed to settle claims that the bank over-charged active or recently active military service members

Credit card holders - $1,200,000,000

In October 2012, JPMC paid $1.2 billion (20% of a global $6.05 billion settlement) to settle claims that it, along with other banks, conspired to set the price of credit and debit card interchange fees.

Homeowners - $1,960,000,000

On January 7, 2013, JPMC announced that it and a number of other financial institutions entered into a settlement to make a cash payment of $760 million into a settlement fund for qualified borrowers.

Consumers - $389,000,000

In September 2013, JPMC agreed to pay $80 million in fines and $309 million in refunds to consumers who were billed for credit monitoring services that the bank never provided.

Madoff victims - $3,054,000,000

In January 2014, JPMC agreed to forfeit to the federal government $1.7 billion (as a non-tax-deductible payment) as part of a Deferred Prosecution Agreement relating to its failure to comply with the requirements of the Bank Secrecy Act with respect to Madoff’s brokerage account.

JPMC also paid a $350 million Civil Money Penalty to for violating the Bank Secrecy Act. JPMC also paid a $461 million Civil Money Penalty for failure to detect and adequately report suspicious transactions conducted by Madoff. JPMC also paid $218 million to settle a class action brought by Madoff victims. JPMC also paid $325 million to settle claims brought by the Madoff trustee.

Mortgage-bkd securities - $4,500,000,000

On November 15, 2013, JPMC announced it had reached a $4.5 billion agreement with 21 major institutional investors to resolve claims related to mortgage backed securities.

LIBOR victims - $109,000,000

On December 2013, JP Morgan reached a settlement with the European Commission regarding its Japanese Yen LIBOR investigation concerning antitrust rigging of benchmark interest rates.

Checking accounts - $110,000,000

In February 2012, JPMC agreed to pay $110 million to settle claims that it over-charged customers for overdraft fees.

JPMC shareholders - $1,020,000,000

In September 2013, JPMC paid $920 million in fines to settle claims of mismanagement with respect to its oversight of traders involved in the “London Whale” disaster which caused losses of approximately $6 billion. In addition, JPMC paid a $100 million fine for reckless conduct and market manipulation.

Consumers of electricity - $410,000,000

In July 2013, JPMC paid $410 million to settle claims of bidding manipulation of California and Midwest electricity markets.

Veterans - $659,000,000

In March 2012, JPMC paid t a $45 million fine to settle charges that it charged veterans hidden fees in mortgage refinancing transactions.

Invalid Insurance Claims - $614,000,000

In February 2014, JPMC agreed to pay $614,000,000 to settle charges for invalid insurance claims that have been paid to JP Morgan Chase since 2002 through the date of settlement.

Collateralized debt - $153,600,000

In June 2011, JPMC paid a penalty to the SEC of $153.6 million to settle charges that it failed to disclose material information to investors in collateralized debt obligations.

Municipal bond buyers - $228,000,000

Municipal bond transactions in 31 states, generating millions of dollars in profits.

The American people - 88,300,000

In August 2011, JPMC paid the Treasury Department $88.3 million to settle claims that it improperly processed transactions in violation of sanctions laws against Cuba, Iran and the Sudan.

Pension fund investors - $150,000,000

In March 2012, JPMC paid $150 million to settle claims that it imprudently invested pension funds in a risky debt vehicle.

Home mortgagors - $22,100,000

In December 2013, JPMC paid $22.1 million to settle a lawsuit alleging that the bank imposed expensive and unnecessary flood insurance on homeowners whose mortgages the bank serviced.

JPMC customers - $20,000,000

In April 2012, JPMC paid $20 million to settle claims that it commingled customer funds that it was required to keep separate.

Great Britain regulators - $48,600,000

In June 2010, JPMC paid for failure to maintain required separation between customers’ accounts.

Money market funds - $25,000,000

In July 2010, JPMC paid $25 million to settle claims that it sold unregistered securities to a state-run municipal money-market fund that suffered a run on deposits because it held defaulted debt.

Municipal bond investors - $43,000,000

In December 2012, settled for $43 million for alleged antitrust violations in the market for financial instruments related to municipal bond offerings.

Mortgage investors - $296,900,000

In November 2012, JPMC paid $296,900,000 to settle claims that the bank misstated information about the delinquency status of mortgages that served as collateral for a securities offerings underwritten by the bank.

Mortgage-backed securities - $13,000,000,000

$13 billion settlement with JPMC to resolve “federal and state civil claims arising out of the packaging, marketing, sale and issuance of residential mortgage-backed securities JPMC agreed to pay $13 billion in exchange for complete civil immunity. The DOJ did not disclose the identity of a single JPMC executive or employee responsible for its actions and did not require JPMC to take any remedial measures to ensure that the conduct is not repeated.

Fannie Mae/Freddie Mac - $1,100,000,000

On October 25, 2013, JPMC agreed to resolve, for $1.1 billion, litigation with Fannie Mae and Freddie Mac concerning mortgage repurchase obligations.

Mortgage-bkd sec invstrs - $280,000,000

Settlement of $280 million to resolve claims against JPMC that it misled investors in billions of dollars’ worth of mortgage backed securities.

General public - $650,000

To settle charges brought against it filed inaccurate reports with the CFTC from 2012 and continuing even after the charges were brought against JPMC.

Schemes of a Financial Investment Firm - The Silver Lining

In my experience and observation of financial investment firms over the last 3 decades, I do not believe that JPM is any worse than any other multi-billion dollar financial investment firm or insurance company. You can google the name of your “favorite” financial institution with the name followed by the words, “fines and penalties.” This short exercise will provide insight into the type of financial investment firm you have entrusted with your money.

The government cannot stop this behavior but you can. Close your account. Do you think you have been harmed by the practices in the financial services industry toward the public? Leave a comment below and share with other readers.

To read more details about any of the above fines against JP Morgan Chase: more details about these fines and penalties.

Leave a Reply