Do Not Rely on Stock Performance for Immediate Retirement Income

I have the good fortune of experience. When it comes to investing, age helps. I have observed decades of ups and downs in the stock market. My main observation is that the market often has losing periods or bear markets. Yet after those declines, the stock market climbs higher than before. While this may not happen in the future, the probability is that the same pattern will repeat again and again -- that today’s lower stock prices will be followed by record-high prices.

During every bear market, I see a rash of articles concerning retirees and their panic about their declining stocks. There would be no panic if the following simple concept were understood and applied. You cannot rely on the stock market performance for current or short-term retirement income. The stock market is a long-term vehicle and should only be used for long-term purposes.

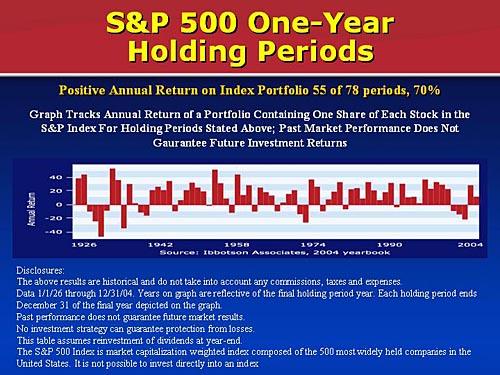

Let me provide an example. Historically, if you take any one year, there is a 70% chance that the stock market will rise in value. But there is a 30% chance you will lose money. The simple conclusion is this: to "bet” on the stock market’s performance in any single year is treating the market as a gambling casino. The stock market is not a reliable provider of positive returns over a one-year period.

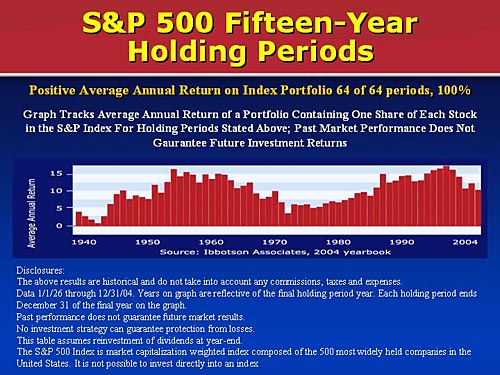

However, if we look again at history, we see that over any 15-year period, the stock market has produced a positive return. The simple conclusion is that investing in stocks for the long run is a low-risk way to get positive returns. Does that mean you must hold your stocks for 15 years? No.

How to Use Stocks for Retirement Income

It means that you cannot rely on the performance of stocks or stock mutual funds for immediate income. You must have other sources for immediate income so that you can choose when to sell stocks and use the gains for income.

Let’s take an example. Say you have $600,000 of retirement assets. You need $2,000 per month in immediate retirement income. One way to accomplish this:

- you invest $400,000 in fixed income instruments paying 6% = $2000/month income

- the remaining $200,000 you can invest in stocks because you will not be depending on them in the short run

You will remove money from your stock portfolio after a period of positive performance, say after three years in a row of gains (the S&P 500 commonly has 3 years in a row of positive performance - since 1973, there have been 24 occurrences of positive performance 3 years in a row). You remove your gains and place those gains into fixed income instruments that provide consistent current income. The key here is that you never need to touch your stock portfolio in a bear market. You harvest your gains after the positive performance of stock prices and do not sell during bear markets.

This is called a two-bucket strategy. You have one bucket that provides immediate income and another bucket that provides long-term growth. You can of course refine this and add complexity by having three buckets. For example, one bucket would be for your income needs in the next one to four years, a second bucket invested to be harvested in years four through eight, and then your stock portfolio would be harvested only after eight years and after gains have been achieved and ready to harvest.

Stagflation

You may be too young to remember stagflation. But it appears that we are headed into a similar scenario to 1973/1974 when the economy stagnated and inflation was simultaneously high. The stock market decline was very steep. The recovery was also steep. The lesson - stock investing is not for the short term. If you need assets for immediate expenses, stocks or stock mutual funds are the wrong place.

| Year | Standard and Poors 500 Performance |

| 1973 | -15.00 |

| 1974 | -26.00 |

| 1975 | 37.00 |

| 1976 | 24.00 |

SEND ME THE INFIORMATION