Good news. Most retirees pay tax on dividends at a very low rate. Retirees benefit from several senior tax breaks and we will devote a post each one of these in our "senior tax break" series.

As research indicates, people age 60+ own more dividend paying stocks than those in younger groups, so any tax advantage on dividends becomes a senior tax break:

We study thestock holdings of more than 60,000 households and find that as a class, retail investors prefer non dividend paying stocks.....For holdings of dividend paying stocks, among retail investors we identify a preference for dividend yield that increases with age (consistent with life cycle or consump-tion preferences) and decreases with income (consistent with low tax investors holding high yield stocks).

[1. Do Dividend Clienteles Exist? Evidence on Dividend Preferences of Retail Investors John R. Graham and Alok Kumar The Journal of Finance, Vol. 61, No. 3 (Jun., 2006), pp. 1305-1336]

One page "invest like the rich" cheat sheet provides short explanations of how the rich investment differently. You don't need to be rich to copy what they do. Download now.

What Rate is Used to Pay Tax on Dividends?

Normal dividend income is included to your other gross income. After deductions and exemptions, your resulting 'taxable' income is subject to taxes at the income tax rate for your filing status. These tax rates have tax brackets that run from 0% to 39.6%, based on how much taxable income you have.

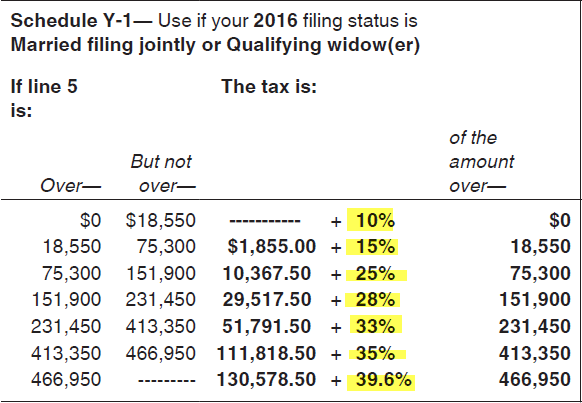

For 2016, here are the tax brackets for married couples for each taxable income range highlighted in yellow:

Tax Rate Table 2016

But on dividends, you pay a lower rate than the above table indicates. You pay tax on dividends based on your total income but at a lower rate than other income as we explain. Even though you could pay as much as 39.6% federal tax on your regular income, dividend income caps out at 15%.

Rate at Which You Pay Tax on Dividends 2016

| Investment tax rates versus Income tax rate | |

| Tax rate on net long term capital gains and qualified Dividends | If 'taxable' Income tax rate bracket (from above table): |

| 0% | Less than 25% |

| 15% | At 25% or higher |

| Filing Status determines where 25% income tax begins | |

| For filing status | 25% Income tax rate begins at |

| Single: | $37,650 |

| Married Filing Jointly: | $75,300 |

Tax rates on qualifying dividend income (as well as net long term capital gains) might be as low as 0%, based on whether or not your taxable income tax rate falls below the 25% bracket. The table shows the taxable income for the filing status that puts you at the 25% income rate. Beneath that taxable income, your certified returns are tax free; at or above it they're taxed at only 15% (These rates currently continue through 2016).

Let's take a quick example of Marty and Susan Smith, both age 62 and retired. Their total annual income from all source is $90,000. Of course, they don't pay tax on this amount. They pay tax on their taxable income as shown here:

| Gross income | $90,000< |

| 2 Exemptions | $8,100 |

| Standard Deduction | $12,600 |

| Taxable Income | $69,300 |

If you look above at the tax rate table, you can see that highlighted in yellow, Mart and Susan are in the 15% tax bracket. And then, if you look to see the rate at which they pay tax on dividends on that table above, you see that their dividend tax rate is 0%. YAHOO!

You can therefore see that one can have a respectable income and pay 0% or not more than the 15% tax rate on dividends.

Exceptions to the Above Tax Rates on Dividends

High Income taxpayers pay a higher tax rate on dividends:

- Dividends are taxed at a 20% rate for taxpayers whose income surpasses the 35% tax bracket

- Nonqualified dividends are taxed at the same rates as ordinary income (currently a 39.6% maximum).

- Single taxpayers with Modified Adjusted Gross Income (MAGI) of $200,000 and married couples with MAGI exceeding $250,000 are also subject to a 3.8% Medicare surtax on net investment income (which includes all taxable dividends).

Let's mention one more issue. The discussion above refers to qualified dividends meaning you are not trading these dividend stocks actively. Specifically, a qualified dividend is a dividend on common stock that you must have held for more than 60 days during the 121-day period that begins 60 days before the ex-dividend date. Rather than make your eyes roll back in your head with technicalities, the details on qualified dividends are here with examples.

You pay tax on dividends that are non-qualified at the same rate as all other income.

Dividends from Preferred Shares

Dividends on "true" preferred shares also get preferential tax treatment as long as they are qualified dividends. For preferred stock, a qualified dividend requires you to hold the stock more than 90 days during the 181-day period that begins 90 days before the ex-dividend date if the dividends are due to periods totaling more than 366 days.

Be careful as some preferred shares are not true preferred shares and have dividends taxed as ordinary income. Ther are called Trust Preferred Securities. So make sure that before you buy, you know if you are buying a Trust Preferred Security or a true preferred. Common names for these are:

CBTCS™(Corporate Backed Trust Certificates), CORTS™ (Corporate Backed Trust Security), MIPSSM (Monthly Income Preferred Shares), MIDSSM (Monthly Income Debt Securities), PCARS (Public Credit and Repackaged Securities), PPLUSSM(Preferred Plus Trust), QUICSSM (Quarterly Income Capital Securities), QUIDSSM(Quarterly Income Debt Securities), QUIPSSM (Quarterly Income Preferred Securities), TOPrS™ (Trust Originated Preferred Securities), TRUPS (Trust Preferred Securities).

You may already own these and they were sold to you as "preferred shares" which they are not.

Leave a Reply