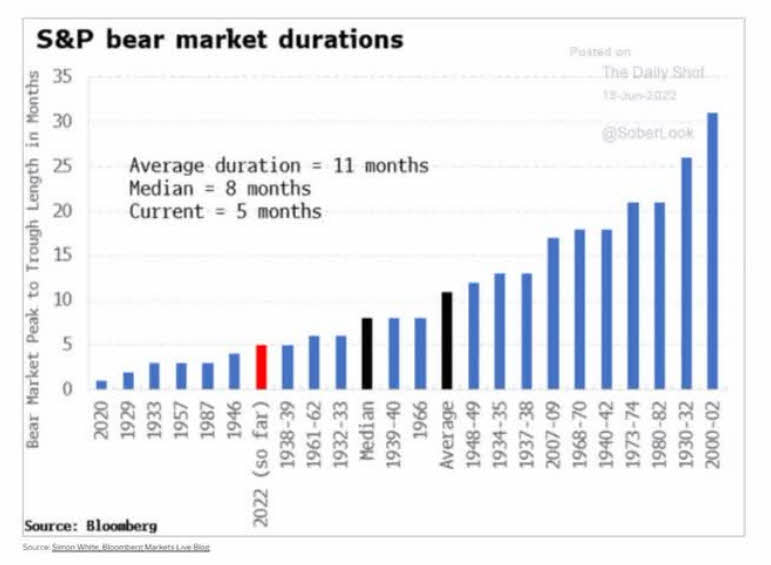

Bear Market Typically Ends Sooner Than People Expect

The average bear market lasts 11 months. The one which occurred in 2000 (the dotcom crash) lasted 30 months.

Given the frequency of bear markets (about once every 5 years), it is surprising that people get alarmed or concerned when they occur.

A stock market investor getting word about bear markets is like a Florida resident getting worried about hurricanes. They come frequently and there is no way to avoid them. They are part of being a stock market investor. You will never be able to forecast them and get out of the market and then get back in the market at the right time. Market timing is a fool's game. That has been proven again and again.

Warren Buffett does not try and time the market. If anyone has enough money to hire a thousand finance PhD's and get the smartest geniuses working for him, he would've uncovered some methodology for avoiding bear markets. He has not.

So please, put on your big boy pants and stop whining. The stock market rewards people for longevity in patience. If you are not patient, do not invest in stocks.

Reversion to the Mean

Investing in the S&P 500 index earns you 10% per year. Some years will be higher in some years will be lower. But let's say that you have three years in a row averaging 15%. The principle of reversion to the mean tells you that since you have just experienced a period of above-average returns, you must expect a period of below-average returns so that the average will remain at 10% annually.

What do you notice from this chart below of the performance of the S&P 500?

Notice that big spikes up are followed by big spikes down. In other words, after a few good years of earning more than 10% annually, you can expect a period of earning less than 10% annually. The really good news is that you see more upward spikes than downward spikes.

Given that bear markets occur, on average, once every 5 years, you might conclude that it would be wise to sell after 4 years of market increases. Unfortunately, that will not work so well. As you can see from the table below, sometimes the market rises for 8 or more years in a row before having a decline.

| Year | Standard and Poors 500 |

| 1973 | -15.00 |

| 1974 | -26.00 |

| 1975 | 37.00 |

| 1976 | 24.00 |

| 1977 | -7.00 |

| 1978 | 7.00 |

| 1979 | 18.00 |

| 1980 | 32.00 |

| 1981 | -5.00 |

| 1982 | 21.00 |

| 1983 | 23.00 |

| 1984 | 6.00 |

| 1985 | 32.00 |

| 1986 | 18.00 |

| 1987 | 5.00 |

| 1988 | 17.00 |

| 1989 | 31.00 |

| 1990 | -3.00 |

| 1991 | 30.00 |

| 1992 | 7.00 |

| 1993 | 10.00 |

| 1994 | 1.00 |

| 1995 | 37.00 |

| 1996 | 25.00 |

| 1997 | 33.36 |

| 1998 | 28.58 |

| 1999 | 21.04 |

| 2000 | -9.2 |

| 2001 | -11.9 |

| 2002 | -22.1 |

| 2003 | 28.7 |

| 2004 | 10.9 |

| 2005 | 4.9 |

| 2006 | 15.8 |

| 2007 | 5.5 |

| 2008 | -37 |

| 2009 | 26.46 |

| 2010 | 15.06 |

| 2011 | 2.11 |

| 2012 | 16 |

| 2013 | 32.39 |

| 2014 | 13.69 |

| 2015 | 1.38 |

| 2016 | 11.96 |

| 2017 | 21.83 |

| 2018 | -4.38 |

| 2019 | 31.49 |

| 2020 | 18.4 |

| 2021 | 28.71 |

How Investors Can Avoid Bear Markets

You can't avoid bear markets so stop thinking about it. If you are a nervous nelly, then do not buy stocks. If you have little patience, then do not buy stocks. Consider however the flip side. A simple trait like patience can make you a financial winner. You do not need to be smart. You do not need to be educated. You simply need to be patient.

If you do not want to think about it, you should buy index funds and never look at the value on your statement or online. Buying individual stocks can be more lucrative. However, it takes more work and some knowledge. OR, use proven formulas such as the Dow Dividend Staryteg, or the Leaders published at Investors.com or the Value Line Rankings.

What Should Retirees Do in Bear Market

Retirees typically get more concerned than others about bear markets. However, their concern is caused by a mistake they made before the bear market started.

You can never rely on short-term performance in the stock market to pay your living expenses. So a retiree who had planned to take X amount of dollars out of their stocks gets really nervous when they see their stocks fall by 30%.

Because stocks cannot be relied on as short-term funding mechanisms. One must either use the bucket strategy or another method to avoid drawing from a stock portfolio in a bear market.

Let's take an example. Let's assume a retiree has a million-dollar stock portfolio. They need to withdraw $50,000 annually to support their lifestyle from that portfolio. They calculated that withdrawing 5% per year ($50,000 /$1 million) would have their money last a long time. But if their portfolio falls in value from $1 million to $700,000, now those annual withdrawals are much larger percentage of the portfolio ($50,000/$700,000 = 7%). The portfolio will be consumed much more quickly. Retirees would be best suited if they could avoid withdrawals during bear markets.

One way to do that is to use margin. Margin allows you to borrow against your stock portfolio without selling any shares. As an example, the retiree could borrow $50,000 from their $700,000 portfolio and not need to sell any shares. The cost of this is rather low, about 3% a year on the borrowed amount. The borrowed amount can be repaid in later years when stock market values increase.

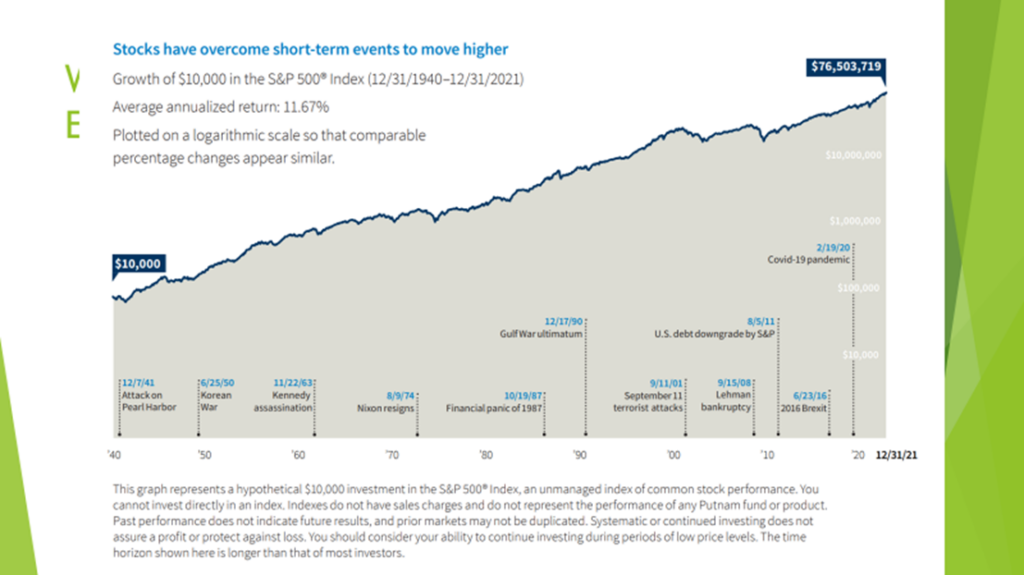

If you are worried that your stock market values may not increase, you should not be a stock market investor. No matter how bad things looked in the past (see image below), amazingly, stocks increased in value.

Him

Leave a Reply