Let’s look at an example; Margaret just turned 62 and her husband is 64. Margaret has not worked for the past 10 years and worked 20 of the last 35 years. If she retires now, she’s entitled to a monthly payment of $400 (after the 25 percent reduction for retirement at the age of sixty-two). When Margaret’s husband retires at the age of sixty-six, in 2 years, his monthly Social Security benefit will be $1,350. Margaret could claim her social security today and receive her $400 per month, based on her own earnings. Then when her husband retires, she could receive a benefit based on his work record. This will come to $472.50, or 35% of her husband’s benefit (see prior table). You may have heard that spouses get 50% of the higher-earning spouses benefit—but that’s ONLY if they wait until their own full retirement age to start collecting benefits.

Decisions for Spouses

Start my own benefits at age 62 |

You can take reduced benefits on your wage record before full retirement age. If you do, your benefit will always be reduced--even if you take reduced benefits on your own record and then take spouses benefits when the higher earning spouse retires (see previous table showing reduction in spousal benefits). |

Start my own benefits at full retirement age |

If you are the higher earning spouse, you always will quality for benefits under your own earnings record and then the decision is when to start benefits as discussed in the previous section |

Start benefits at age 62 based on my spouses social security earnings |

You cannot receive spouse's benefits until your spouse files for retirement. If you choose to receive a reduced benefit before full retirement age, you are not entitled to the full spouse's benefit rate upon reaching full retirement age. A reduced benefit rate is payable for as long as you remain entitled to spouse's benefits. |

Start benefits at full retirement age based on my spouses social security earnings |

If you stopped working for several years or had low earnings, the spouse's benefit may be higher. At full retirement age, a spouse receives 50 percent of what the higher-earning spouse is entitled to at full retirement age. At death of the higher earning spouse, you receive that deceased spouse's full benefit |

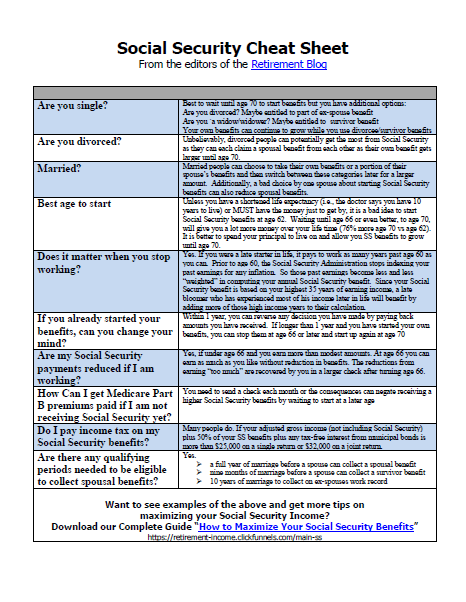

Most people think that they get the largest payment automatically. Not true. You need to make choices when you apply and if you make the incorrect choice, you get a smaller check -- for life. Even if you already receive Social Security Benefits, you may be able to change your selections.

Unfortunately, the federal government likely taxes your social security income and our next article explains how to reduce or eliminate tax on social security income:

Social Security Taxes - How to Reduce Taxation of Your Benefits

Maximize Your Social Security Income

Get the one-page social security Cheat Sheet

You may think that the folks at the Social Security office will tell you how to get the biggest monthly check. In fact, the federal rules PREVENT them from advising you. There are millions of people who have given up more than $50,000 just by making a simple yet incorrect method of taking their Social Security benefits. Don’t let that be you! Get your free copy now.

Hello, I am wondering am I allowed to receive my social security benefits now ( Im 56) my husband is going to retire next year. If I collect my benefits now does this hurt his retire benefits in any way? Please let me know Thank-you Denise

When a worker files for retirement benefits, the worker's spouse may be eligible for a benefit based on the worker's earnings. So you cannot get anything until your husband begins receiving his social security. Another requirement is that the spouse must be at least age 62 or have a qualifying child in her/his care.

I am a retired educator and my husban has minimal social security benefits. Am i able to draw spousal benefits from him. I make a nice retirement incone.I am 63.

the rules are here http://www.ssa.gov/retire2/yourspouse.htm