Social Security Retirement Benefits

Social Security is a government-sponsored pension that most Americans will qualify for at retirement age. A portion of each employee’s income, along with an equal share from the employer, is contributed to the fund throughout that person’s working career. Self-employed people make both the employee and employer contributions.

Will You Qualify?

Nine out of ten American works will qualify to receive benefits either directly, or as the spouse of an eligible person. Some of those not qualified to receive Social Security benefits include:

Most people think that they get the largest payment automatically. Not true. You need to make choices when you apply and if you make the incorrect choice, you get a smaller check -- for life. Even if you already receive Social Security Benefits, you may be able to change your selections.

- Civilian employees of the federal government that were hired before 1984,

- An employee of a state or local government who is:

- A member of their employer’s retirement system;

- and Not covered by a voluntary state/federal Social Security agreement, or

The rules for being considered “fully insured” vary somewhat depending on your age, but a general rule of thumb is that you must have one “credit” for each year you worked after 1950, in which you were 21 years of age or older. You get one credit for each quarter you work in which you earned at least the minimum amount as required by the SSA. For 2003, you earn one credit for each $890 you earn [ii] , up to a maximum of four credits per year.

If you have accrued 40 credits over your work history, you are fully insured and may qualify for a number of Social Security programs including the retirement plan, Supplemental Security Income (SSI) and/or Social Security Disability. Each program has specific qualifications. You can obtain more complete information from the SSA’s website: www.ssa.gov, or from your financial advisor.

The Retirement Plan

If you were born during or after 1929, you must have 40 credits to qualify for Social Security retirement benefits. People born before then need fewer credits. In addition to having enough credits, you must have reached a minimum age to collect retirement benefits. There is a minimum age to collect retirement benefits, but if you wait a few years beyond that minimum, you may get a larger payment.

Until a few years ago, you had to wait until age 65 to collect the maximum benefit you are entitled to. Now the age at which you can begin collecting benefits and get the maximum payment depends on when you were born.

Age to Receive Full

Retirement Benefits

[iii]

|

|

|

|

1937 or earlier |

65 |

|

1938 |

65 and 2 months |

|

1939 |

65 and 4 months |

|

1940 |

65 and 6 months |

|

1941 |

65 and 8 months |

|

1942 |

65 and 10 months |

|

1943-1954 |

66 years |

|

1955 |

66 and 2 months |

|

1956 |

66 and 4 months |

|

1957 |

66 and 6 months |

|

1958 |

66 and 8 months |

|

1959 |

66 and 10 months |

|

1960 and later |

67 years |

You may get a bigger payment by delaying your retirement. Whether or not this is a good idea requires careful analysis. Some people may be better off beginning payments earlier than the maximum benefit date, even if the amount is lower. Check with your advisor to determine what is best for your situation.

How much can I expect?

The best way to get this answer is to review the annual statement that the SSA sends out to every worker over 25. This estimate is likely to be the most accurate, as the formula to figure benefits can be complicated. You should receive a copy of this statement each year, about 3 months before your birthday.

You also can request a statement by calling Social Security and asking for a form SSA-7004, Request for Social Security Statement, or by downloading the form at www.socialsecurity.gov/online/ssa-7004.html on the Internet. Or, you can calculate your benefit yourself using the programs available at www.socialsecurity.gov/retire2 on the Internet.

To figure your benefit, the SSA averages your total earnings over your working career. They then adjust this number to reflect changes in average income since you earned it. They then calculate an average monthly earning based on your highest 35-year period of employment. Then a formula is applied to this number to arrive at a base benefit, also called your primary insurance amount (PIA). This is what you would receive if you began your benefits at your full retirement age (see above chart).

You may or may not actually receive the PIA. Factors that may increase or decrease this amount include retiring before your full retirement date, delaying your retirement (up to a maximum of age 70), and cost of living increases that should occur over time. If you are a government employee and receive a pension, a different formula may apply. You may also be eligible for SSI benefits if you are disabled.

Qualifying as a Spouse

If you have worked and paid Social Security taxes, you may qualify for your own pension or qualify as the spouse of a recipient. You can receive benefits as a spouse if you are over age 62 or have dependent children 16 or under, or a disabled child over 16. In addition to those requirements, you must also not be eligible to receive your own Social Security pension in an amount greater than half of your spouses.

Let me illustrate:

|

|

|

|

|

|

$2000 mo |

$1000 mo |

$1200 mo |

no |

|

$2000 mo |

$1000 mo |

$800 mo |

yes |

Of course this is a government agency, so nothing is ever as simple as it seems. The typical spousal benefit is half of the eligible retiree’s benefit, but there are certain conditions when you may be entitled to less. One situation in which this might occur is if you have children who are also eligible and you reach the family maximum.

If you are entitled to your own pension, you will collect either yours, if it is equal or higher than your spouse’s, or the difference between yours and theirs, on top of your own benefit.

If you are divorced you may still be eligible to collect as a spouse provided you have not remarried and your former spouse is eligible. You must also have been married for at least 10 years.

If you are a widow or widower, and are age 60 or above (50 if disabled) you can collect on your former spouses Social Security. When you reach age 62, you can decide to switch to your own Social Security benefit if it will be larger.

What you qualify for will depend on your situation, and this guide is just an outline. There may be circumstances that prevent your eligibility. Your financial advisor, or a counselor at the SSA, can answer your questions.

Taxation of Social Security

It seems unreasonable that Social Security income is taxed given it’s a benefit received on income already taxed, but it can be subjected to income taxes if your total income is above a certain limit.

If your modified AGI (adjusted gross income) plus one-half of your Social Security benefit is above $25,000 if you are single, or $32,000 as a married couple, your benefit may be taxable. If you are married, living with your spouse, but file separately, your benefit may be taxable from the first dollar received. Note that the term “modified AGI” includes your AGI plus any tax-exempt bond interest.

How much of it will be taxed? If you are married and file jointly, and your combined income plus benefit exceeds $44,000, or are single and it exceeds $32,000, up to 85 percent of your benefit may be taxed.

Detailed income planning, savings vehicles such as Roth IRAs, annuities and life insurance, and which assets you use to derive your income may reduce the amount of actual income you must include in your AGI calculation used to determine the taxability of your Social Security benefit. Consult with your tax or financial planning expert to determine the best way to balance your income and your tax liability.

Where to get More Information

This article is only a generalized outline of how Social Security works. Your specifics may be quite different. For more information, you can visit the Social Security Administration’s website at www.socialsecurity.gov, where you can download the Social Security handbook. You should also discuss your situation with your financial advisor as they are best equipped to assist you in determining what you will qualify for, and when you should begin payments. Lastly, keep in mind that no matter when you decide to file for your retirement benefits, you should file for your Medicare benefits before you turn 65 (you will be automatically enrolled if you are collecting Social Security benefits prior to then).

Social Security Handbook

www.ssa.gov

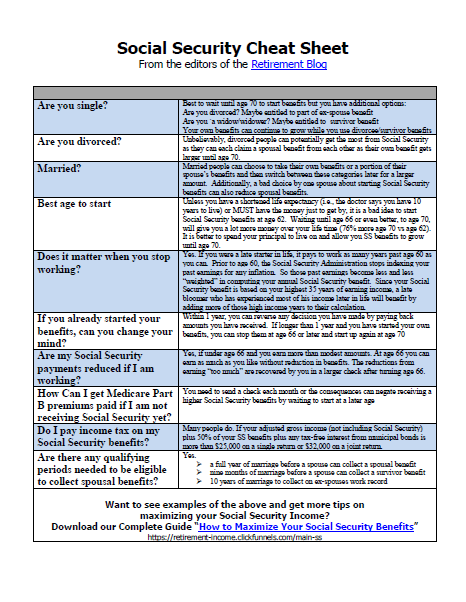

Maximize Your Social Security Income

Get the one-page social security Cheat Sheet

You may think that the folks at the Social Security office will tell you how to get the biggest monthly check. In fact, the federal rules PREVENT them from advising you. There are millions of people who have given up more than $50,000 just by making a simple yet incorrect method of taking their Social Security benefits. Don’t let that be you! Get your free copy now.

Leave a Reply