This is a really straight forward question and if the math were the only factor, here’s the straight forward answer: wait until full retirement age to take your social security income. Below is the table of full retirement ages and the reductions for starting social security income payments early.

No matter what your full retirement age is, you may start receiving social security income benefits as early as age 62.

|

||||||

|

|

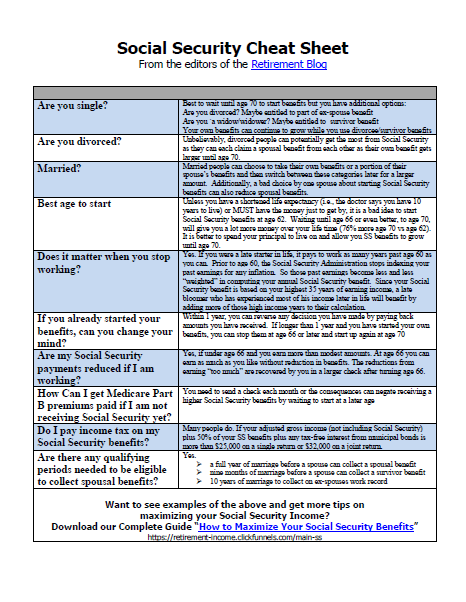

Do You Know How to Get the Largest Social Security Check?

Learn to use the government rules to get the largest payment due you

Most people think that they get the largest payment automatically. Not true. You need to make choices when you apply and if you make the incorrect choice, you get a smaller check -- for life. Even if you already receive Social Security Benefits, you may be able to change your selections. |

Reduction Months |

|

|

|

|

1937 or earlier |

65 |

36 |

.555 |

20.00 |

.694 |

62.50 |

1938 |

65 and 2 months |

38 |

.548 |

20.83 |

.679 |

62.92 |

1939 |

65 and 4 months |

40 |

.541 |

21.67 |

.667 |

63.34 |

1940 |

65 and 6 months |

42 |

.535 |

22.50 |

.655 |

63.75 |

1941 |

65 and 8 months |

44 |

.530 |

23.33 |

.644 |

64.17 |

1942 |

65 and 10 months |

46 |

.525 |

24.17 |

.634 |

64.58 |

1943--1954 |

66 |

48 |

.520 |

25.00 |

.625 |

65.00 |

1955 |

66 and 2 months |

50 |

.516 |

25.84 |

.617 |

65.42 |

1956 |

66 and 4 months |

52 |

.512 |

26.66 |

.609 |

65.84 |

1957 |

66 and 6 months |

54 |

.509 |

27.50 |

.602 |

66.25 |

1958 |

66 and 8 months |

56 |

.505 |

28.33 |

.595 |

66.67 |

1959 |

66 and 10 months |

58 |

.502 |

29.17 |

.589 |

67.08 |

1960 and later |

67 |

60 |

.500 |

30.00 |

.583 |

67.50 |

|

||||||

So let’s take this hypothetical example:

You were born in 1945 and just turned age 62 in 2007. Your full retirement age is 66. You are projected to receive $1500 social security income monthly at that time. However, you could start your social security benefits now at age 62 and receive $1125 (25% reduction). So do you wait and get $1500 monthly at age 66 or take $1125 now at age 62? Assuming that your personal “discount rate” for money is hypothetically 6% and that you view yourself as having average life expectancy, you would come out $3,000 ahead by starting payments at age 62 (this calculation can be done using any financial calculator or spreadsheet with a present value function and the above assumptions). In other words, using these assumptions, it will only make a $3,000 difference over your expected life time.

Because there is more to life than your life expectancy and discount rate, here are the other factors to consider:

Issue |

This would argue to…. |

| If you think you can earn more than 6% annually | Take the money now |

| If people in your family tend to outlive the average life expectancy | Take the money later |

| If you need the money to live on now | Take the money now |

| If you are married and your spouse is also dependent on the payments | Takes a lot more figuring – call us on this one |

| Your tax bracket will be lower later | Take the money later |

| Will you have earned income prior to your full retirement age forcing you to forfeit some of your social security benefits | Take the money later |

Once you start to consider several of these factors at once, you may get a headache. Unfortunately, there is no blanket answer as to when to begin social security income payments to maximize the benefit. This is an issue you can calculate and a retirement calculator is provided on this site.

What about your spouse? Read the next article:

Social Security Benefit for Spouses

Maximize Your Social Security Income

Get the one-page social security Cheat Sheet

You may think that the folks at the Social Security office will tell you how to get the biggest monthly check. In fact, the federal rules PREVENT them from advising you. There are millions of people who have given up more than $50,000 just by making a simple yet incorrect method of taking their Social Security benefits. Don’t let that be you! Get your free copy now.

my boyfriend will retire in 2 yrs which he will 62....my question is, does he or can he get extra ssi for having 2 minor kids....at that time of him retiring the kids will b 10 and 13...thank you

you need to look on the social security web site ssa.gov

I turn 64 in September 2017 (retirement age is 66) as my unemployment from a layoff runs out in October 2017.

I worked for 4 months in 2017 earning $43,000 plus $6,000 of taxable income in 2017.

My last 12 years of SS income were much higher than my early life and will increase my benefits.

The guess is that I should file my 2017 to get that SS total average income a little higher.

I should be able to make $16,000 a year consulting.

The wife is 8 years younger and will continue working at $26,000 a year (with benefits).

My Pension plan was wiped out for all practical purposes. My 401K is only $70,000 after 2007.

The house has $250,000 in equity with payments of $1,150.00 a month.

We have no other debts other than the house. We could downsize to lower house payments to $700.

What is missing from the discussion is medical payments under Obamacare.

If one sells the house, or if the stock happened to go up and sell for a profit, does that come out of the above $26,000 SS Payment deduction?

When can my Medicare start and how will that affect my medical payments?

For something that is common, the government SS sites are very generic cookie-cutter and don't really answer questions for the total picture.

You want to get some detailed assistance from a local financial advisor who has expertise in social security consulting. If you go to this link and order this booklet on social security, your contact information will be passed to a local financial advisor who will offer to assist you: http://bit.ly/2t7wujm