There is hype about retirement savings and not having enough.

Saving for retirement is fine, it’s even good but its hype.

Wall Street wants to promote this idea to save more. The more you save, the more you place into the 401ks they manage, the mutual funds they manage, the ETFs they manage and the brokerage accounts they manage.

And all of that management means MORE MANAGEMENT FEES. So the folks who work in any sector of the financial services industry certainly want to encourage your retirement savings.

What about the journalists who write all those stories about retirement savings? What’s in it for them? Nothing. But who do you think they interviewed for their story? A guy from Wall Street. Sadly, much that journalists write about is influenced by the sources of their information.

Again, I think saving is just fine. But the idea that savings can be the bedrock of retirement is overhyped for several reasons.

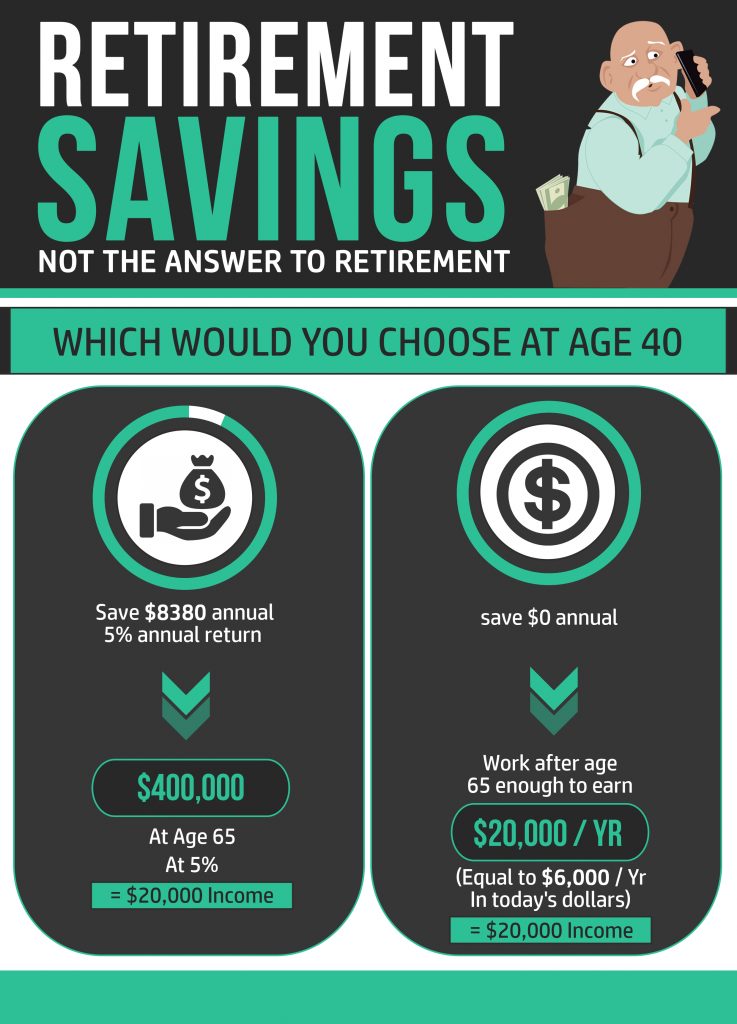

Diligent Retirement Savings Does Not Guarantee a Comfortable Retirement

Just because you save a lot doesn't mean you'll have a big nest egg at retirement.

I met a guy years ago who was 60-years-old. He explained his sure-fire retirement plan. He owned a diversified portfolio of natural resource stocks, everything from oil to mining and related companies. In his mind, this was a sure-fire plan as during his lifetime, natural resources had always climbed in value.

On top of that, everyone knew that the world was running out of oil and other minerals. The amount of minerals in the ground is finite, therefore, they can only rise in value as population increases. The limited supply is true of common elements such as gold to rare-earth minerals monopolized by China. The plan was a safe bet for obvious reasons until the world encountered deflation starting in 2011 (yes, we have been experiencing deflation for 5 years now).

During deflation, the price of natural resources decline. This has occurred for oil, copper, natural gas, rare-earth minerals, coffee and other agricultural commodities. That sure-fire natural resources portfolio is now in the crapper.

Even if you count this guy as stupid, what’s so immune about your portfolio that it will have much value at retirement? What if you happen to reach retirement in years like: [1]

- 1972 to see your S&P 500 indexed portfolio decline by 40% over the next 2 years or

- 1999 to see your S&P 500 indexed portfolio plummet by 43% over the next 3 years (or worse if you owned technology stocks) or

- At the end of 2007, just in time for the housing bubble to burst and see the S&P 500 drop by 36% in a year

You say “Wait a minute, Larry, you cherry-picked those terrible years just to show a few miserable years which are not indicative of the long term.”

You are correct! Paul Merriman, a very insightful portfolio manager, has studied all of the 40-year investing periods since 1928. He found that the worst 40-year period still produced a compounded return of 8.9%.[2] So you feel pretty darn confident, as a 25-year-old, that the plan to save a healthy amount, buy and hold, will get you a multi-million-dollar nest egg.

Hold on there young fella (gals included). We need to consider another problem.

You will not buy and hold.

How People Trash a Diligent Retirement Savings Program

There will be world events that leave you shakin’ in your boots and convince you that the financial world is coming to an end. If you haven’t experienced one of these events yet, you’re in for a lesson about your own emotional stability.

For those who will admit it, the financial world appeared to be at an end in 2007. The facts that the head of the Federal Reserve called the head of every major bank to an emergency meeting and global liquidity seized up as Lehman Brothers and Bear Stearns collapsed were sufficient to have the most savvy financial minds conclude this was the end of economics as we know it.

If you weren’t investing money at the time, it’s hard to understand the emotional toll.

Or you might consider 1987, my second year as a stockbroker, when the market fell 23% on one October day. Close your eyes and pretend that you wake up on a Monday, glance at the front page of Yahoo and see the headline “US Market Down 23% since the Open.”

Not only are you shocked by the omission of the Kardashians being the front page story on Yahoo, you are stymied by the amount of your losses since bedtime. Your consternation is further compounded by remnants of a hangover from the weekend.

In your cool and collected current state, you insist that you would have stayed fully invested given your complete certainty that the market would rebound. Give me a break. You would have likely lost control of our bladder or bowel or both.

So we see the second problem of accumulating retirement savings is that people do not have the emotional stability to do it. [3]

Other Impediments to a retirement Savings Plan

Then we have yet another impediment. What if any of these calamities impacted you or your family:

--life or death illness that required expensive drugs not covered by insurance

--serious depression creating the inability to work

--addiction to pills, drugs or alcohol which decimates your career and most other areas of your life

--natural disaster such as earthquake, fire, flood, hurricane or tornado that destroys everything you own and puts you in a hospital bed for three months

You think this stuff happens only on TV? This author had his house go up in flames along with 2300 others during the Berkeley Firestorm in 1991. So I can speak with experiential authority—shit happens.

Okay, let’s say I am full of it. You know you are immune to the issues I have raised:

- The market doing poorly at the wrong time in your journey to retirement

- Your emotional control (surpassed only by Mr. Spock) in light of financial calamity

- Injury, harm or other catastrophes which impact millions of lesser humans annually

Consider also the fact that you sidestep every one of these potential occurrences. You make it to retirement with an inflation-adjusted $2 million dollars. You recall this post and think “Klein was so full of BS.” And then you get diagnosed with Alzheimer’s.

Here’s my point. While I think savings is laudable, even commendable, its benefits are hyped.

Consider that you have significant control over your retirement years in the years preceding and after age 65. You can still have some great golden years even if you reach that stage with a meager nest egg.

I am still an advocate of saving for the future. But realize that saving is not the be-all of a retirement that works.

Related posts:

Save More for retirement- Not the Answer to Retirement Crisis

Sae More for Retirement - a Stupid Idea

[2] Understanding performance: The S&P 500 Index

[3] In 2001 Dalbar, a financial-services research firm, released a study entitled "Quantitative Analysis of Investor Behavior", which concluded that average investors fail to achieve market-index returns. It found that in the 17-year period to December 2000, the S&P 500 returned an average of 16.29% per year, while the typical equity investor achieved only 5.32% for the same period - a startling 9% difference! The study has been repeated and the results are essential unchanged in 2015.

every person needs to start early investments. Thank you very much for this amazing blog with nice ideas and thoughts.