Let's take a closer look at senior healthcare costs in

According to the Fidelity Retiree Health Care Cost Estimate, the average retired couple age 65 in 2018 may need approximately $280,000 saved (after tax) to cover health care expenses in retirement. This seems like a lot of money, and on the face of it, could not possibly be true.

Of course, those in poverty will qualify for Medicaid and avoid the costs in this post. But for those of modest means, this expense could spell bankruptcy in rertirement.

The first thing I notice about this senior healthcare cost estimate is the quote per couple. Based on US census data, nearly 20 million of the 47 million people over age 65 (43%), are single. It seems to me that this study could have quoted a total senior healthcare cost of $140,000 per person, but I guess you can scare more people with the larger number. I will use $140,000 per person in the remainder of this post.

Briefly mentioned by Fidelity are some solutions (products and services they sell):

"Consider increasing contributions to your tax-advantaged accounts, especially HSAs (if you have one), which enable tax-free spending on health care in retirement." Since all money management, mutual fund, and Wall Street investment managers earn fees from the money you deposit or invest with them, they will always tell you that a solution is to hand them more money.

Details of Senior HealthCare Costs - Do They Add Up?

How did Fidelity get this estimate of $140,000 per person? Here are their basic assumptions and my comments on these assumptions.

Fidelity says, "The average 65+ retiree today should expect to pay around $5,0001 a year on senior healthcare premiums and out-of-pocket expenses, and should carefully weigh all options."

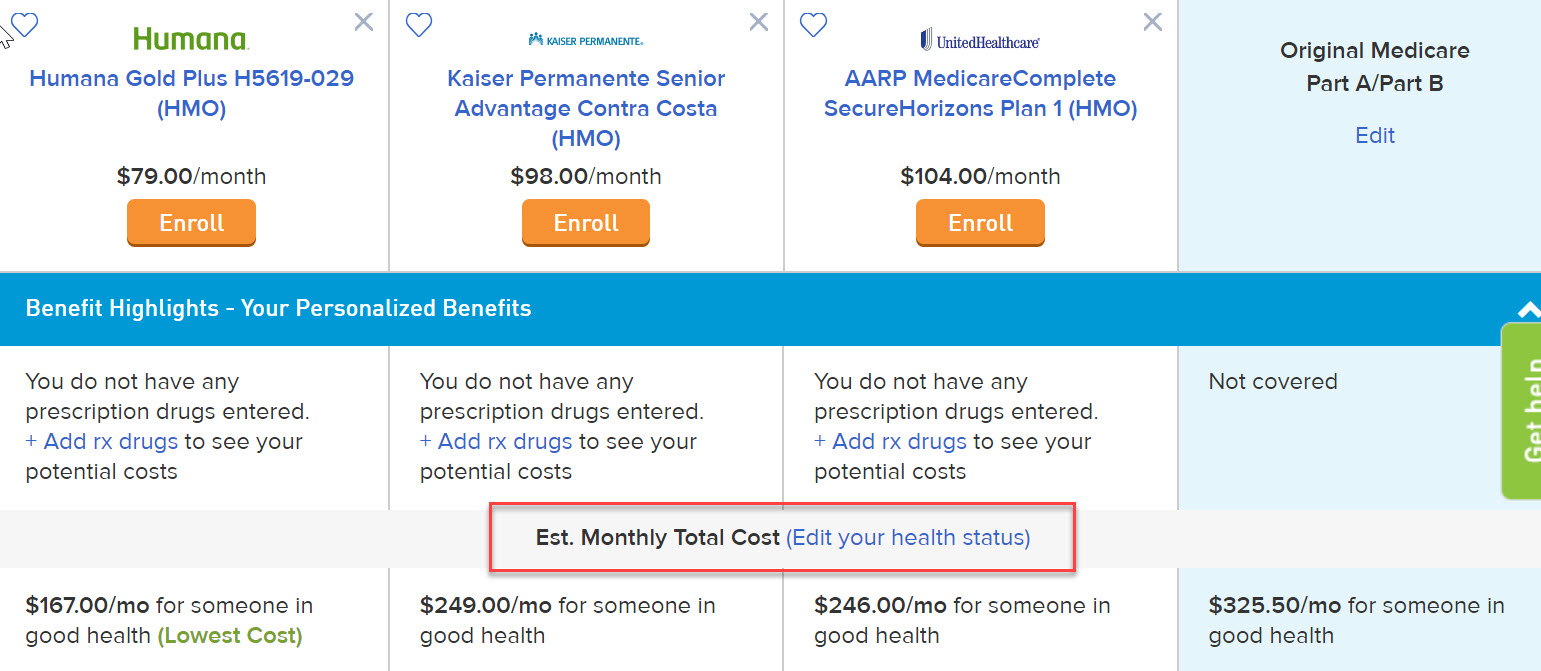

My wife turns 65 in a few months and I have been researching Medicare alternatives. Here are the total monthly out-of-pocket costs for three Medicare Advantage plans in my area.

You can see from the above, each Medicare Advantage plan estimates monthly costs for someone in good health. The estimates range from $167 per month to $249 per month. So for the most expensive Medicare Advantage plan, the yearly cost would be $2,988 (12 months x $249). What if you're not in good health? How would that affect your health?

The nifty

The most expensive plan for an insured in poor health is now $295 per month or $3,540 annually. The cost is higher for poor health, not because you pay more for the Medicare Advantage plan, but because you incur more costs for medication and co-pays.

Do You Also Pay for Medicare

Part B?

We need to add in another senior healthcare cost which is the Part B premium you pay directly to Medicare. Those Part B premiums are based on your income as shown in this table.

So that you will appreciate how much the government subsidizes your healthcare costs, look how much more high-income people pay for Part B. They pay the true cost of the care and the difference between what they pay and you pay, is your government subsidy. If you think you have paid for this through all those years or work and Social Security payments, you have not. The subsidy you get, where does it come from? From the paychecks of your children and grandchildren. Thank them.

When we add the lowest possible Medicare part B premium of $134 per month ($1,608 annually), the total annual healthcare costs for a person in poor health are $5,148 annually ($3,540 calculated above plus $1,608 Medicare part B premium). Therefore, $5,000 a year on health care premiums and out-of-pocket expenses estimated by Fidelity, appears accurate.

Cumulative Cost of Healthcare

After Age 65

To calculate

If healthcare costs are for 20 years at $5,000 per year, that is $100,000. However, we all know that prices increase. So if we assume that your healthcare costs increase 4% annually, here is what happens to the $5,000 annual healthcar cost:

| Age 65 | $5,000 |

| Age 66 | $5,200 |

| Age 67 | $5,408 |

| Age 68 | $5,624 |

| Age 69 | $5,849 |

| Age 70 | $6,083 |

| Age 71 | $6,327 |

| Age 72 | $6,580 |

| Age 73 | $6,843 |

| Age 74 | $7,117 |

| Age 75 | $7,401 |

| Age 76 | $7,697 |

| Age 77 | $8,005 |

| Age 78 | $8,325 |

| Age 79 | $8,658 |

| Age 80 | $9,005 |

| Age 81 | $9,365 |

| Age 82 | $9,740 |

| Age 83 | $10,129 |

| Age 84 | $10,534 |

| Total | $148,890 |

Therefore, the total cost of $140,000 seems to be a realistic estimate for total healthcare costs in retirement.

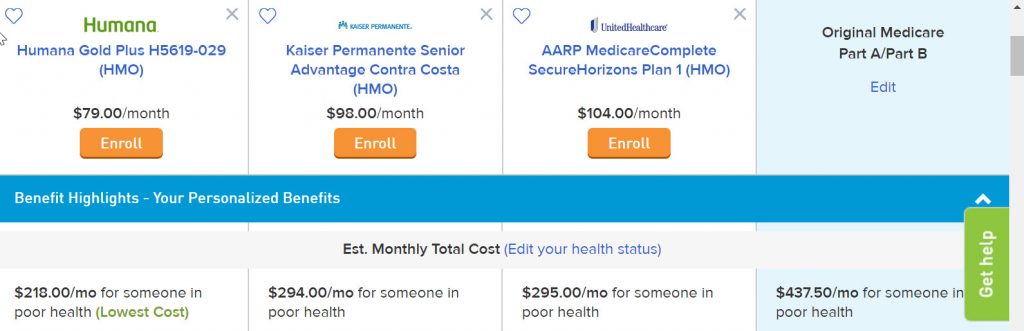

Use a Medicare Advantage Plan instead of traditional Medicare as Advantage plans are less expensive and often have greater benefits. Look at the 2nd table in this post where I show you costs for a person in poor health. The most expensive Medicare Advantage plan has estimated costs of $294 monthly vs $437 monthly for Traditional Medicare.

Best Ways to Reduce Senior Healthcare Costs

Don't be unhealthy. While this may sound silly at first, because you don't think you control your health, you

Medicare Advantage is Better and Will Save You Money

- Many Medicare Advantage plans also include Medicare Part D prescription drug coverage, so you get all your Medicare benefits in one convenient plan.

- You will not

to buy Medigap insurance and have forms and bills as you will with Traditional Medicare - In addition, many Medicare Advantage plans offer coverage for routine vision, dental, hearing services and will even pay for your gym membership so you can stay in shape.

- An emphasis on preventive care.

- Cost controls, including a cap on out-of-pocket costs for physician and hospital services (Medicare Part A and B benefits).

That still doesn't cover all of your health care expenses. There are co-pays and deductibles for all sorts of things.

People that need expensive treatments, like infusions, for cancer or other illnesses, my pay thousands more per year. Also, there are co-pays for Dr. visits and presriptions.

Our out-of-pocket costs, last year, were, $21,800. If that continues and inflates, for 20 years, the total will be very high.

I would encourage you to look for better coverage, either a more comprehensive medigap policy or a Medicare Advantage (HMO) plan. Maybe not available in your area but many seniors belong to Kaiser Medicare Advantage in my area and they have very low out of pocket expenses. My p[ersonal recommendation is always Medicare Advantage as I think the coverage is better with fewer copays, deductibles, forms, etc.

Contradicting- Medicare

Medigap or advantage. I confuse us!

Please order a free copy of this booklet which has a very good comparison (clear and easy to understand) on Medigap vs Medicare Advantage.

https://request.retirementincome.net/landingpage-pat